硅谷Fintech观察③|卖铲子的人:Stripe、Adyen、AirwallexSilicon Valley Fintech Watch ③ | Selling Shovels: Stripe, Adyen, Airwallex

Translated from the Chinese original, first published on WeChat「世像」on July 15, 2026.本文 2026.07.15 首发于微信公众号「世像」。

「为什么中国出不了 Stripe」系列 · 第三篇

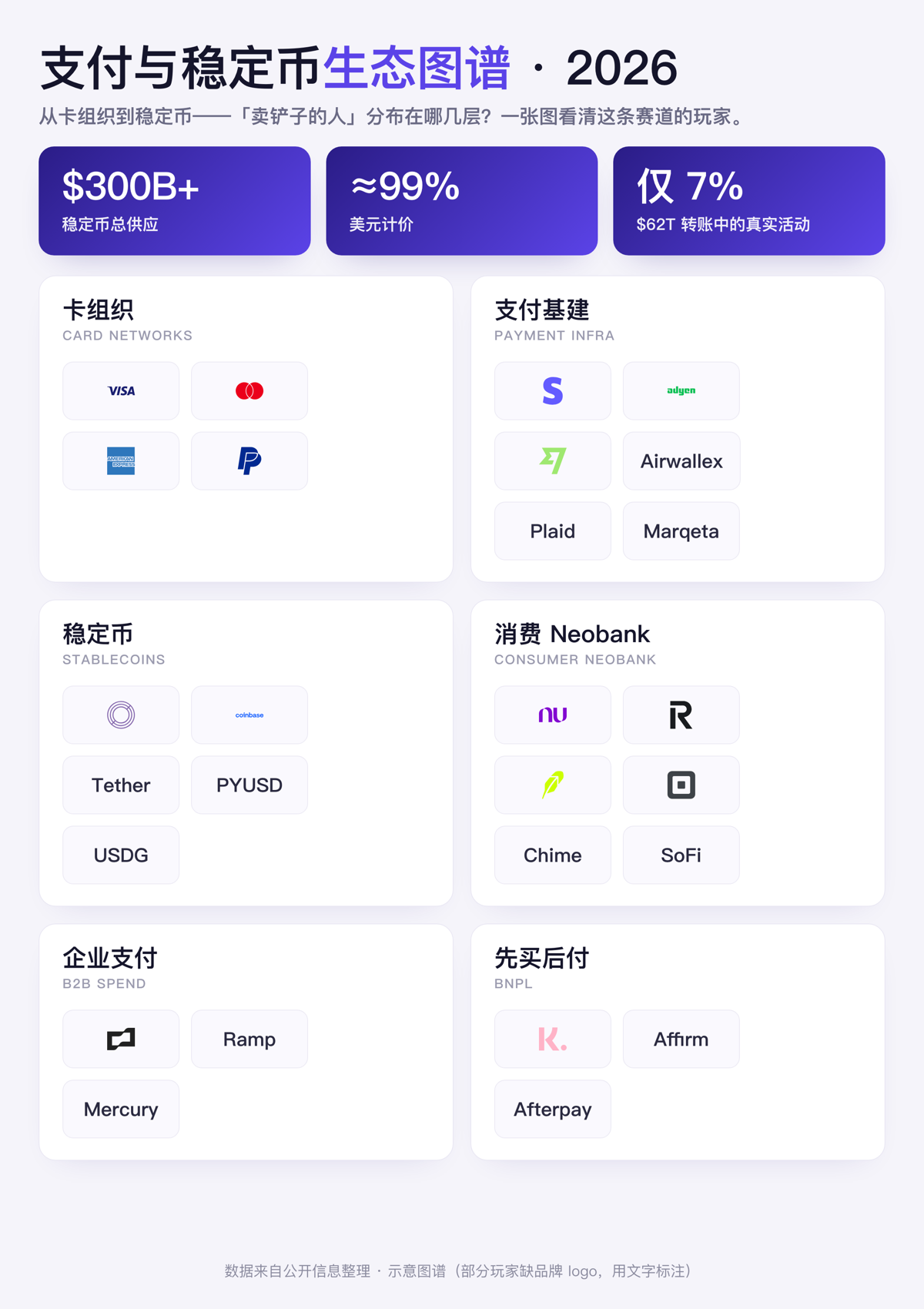

导读|每一百块钱在互联网上流过,就有两三块被悄悄抽走——抽走它的不是银行,是 Stripe、Adyen、Airwallex 这群“卖铲子的人”。上一篇说过,打银行消费侧的明星大多很惨;这一篇讲赢家:一个用规模和生态卡位,一个用利润率封神,一个用十年和八十五张牌照在亚太铺出全球基建。末了还埋着一颗新雷:稳定币,99% 挂的是美元。

三年前,市场给 Stripe 判的是死刑,用词是“死亡螺旋”。

2023 年,这家公司的内部估值从 2021 年巅峰的 950 亿美元一路被打到 500 亿,报道写它“烧钱、增长失速、500 亿都嫌贵”,连一向看多它的人都开始动摇。

到了 2026 年 2 月,Stripe 最新一轮员工股权交易,把估值定在了 1590 亿美元——比一年前的 915 亿涨了 74%。2025 年它处理了 1.9 万亿美元交易额、同比增长 34%,这个数字相当于全球 GDP 的 1.6%,而且明确“稳健盈利”。连微软都把“相当一部分”交易量切了过来,客户名单上还新添了英伟达和亚马逊。它甚至掏出史上最大的一笔收购——11 亿美元买下稳定币公司 Bridge。

那个被唱衰成“死亡螺旋”的赌注,三年后赌赢了。

这正好给上一篇的结论做了注脚:打银行消费侧的那批明星公司大多在对折、腰斩、退出冰封,而卖铲子的人,在穿越周期。

这篇,我们聊这群“卖铲子的人”——为什么企业支付基建是这条赛道的皇冠,Stripe、Adyen、Airwallex 三个主角各自代表什么,还有一条三年前那批素材里几乎不存在、如今却成了新战场的轨道:稳定币。最后我抛一个问题,把整个系列引向终点:这样一层“卖铲子”的基建,凭什么护城河这么深?而它,又为什么在中国几乎长不出来?

数字尽量用 2026 年最新口径。开始。

一、为什么基建是皇冠:卖铲子的人留得住毛利

先把这一篇的总论点立住,再用交易砸实。

每一场淘金热里,最稳的生意从来不是淘金,是卖铲子。原因只有一个:基建把毛利留在自己那一层,不分给别人。

这条其实不止在金融成立——眼下的 AI 就是同一出戏。2024、2025 年真正闷声赚翻的不是哪个大模型,是卖铲子的英伟达;到了今天,铲子又往上游递了一层,轮到造内存的美光、闪迪、SK 海力士、三星——一颗 AI 芯片的物料成本里,光高带宽内存(HBM)就吃掉一半以上,美光 2026 年的产能甚至早早就卖光了。淘金的换了一茬又一茬,卖铲子的始终在数钱。

最锋利的证据,是同一条赛道里两种命运的估值对照。同样从“企业支出管理”起家——给公司发智能信用卡、顺手把报销和控费自动化——选择做基建的 Ramp,2026 年估值 440 亿美元;而开创了这个品类、却选择卖身的 Brex,被 Capital One 以 51.5 亿美元收购。前者是后者退出价的 8.5 倍。开品类的没赚到品类的钱——是不是挺有意思。

打个比方你就懂了:Stripe 之于互联网生意,就像自来水公司之于一座城。 没人会给自来水公司颁创新奖,但这座城每开一次水龙头,它都在收钱。早年 Stripe 自己有个更狂的说法——它要做“互联网未来增长的 3% 的税”。

(大白话:embedded finance / 嵌入式金融,就是把“账户、支付、放贷”这些原本属于银行的功能,像积木一样塞进任何一个非金融的 App 里;BaaS 则是“银行即服务”——持牌银行把牌照和账户能力批发给金融科技公司去用。)

而 AI 正在让这门“卖铲子”的生意更值钱:它让基建从“帮人做事”升级成“替人做事”。一个例子是给医生诊所做 AI 财务后台的 Lassie,声称能自动完成 98% 的入账——当基建不只是省人力、而是直接把活干完,它能收的钱就完全不是一个量级了。

2019 年那一代金融科技明星,如今已经彻底洗牌:Brex 被 Capital One 收编、Ramp 长成了 440 亿美元的支出基建、Mercury 干脆去拿了银行牌照——三家从同一个赛道起步,走向了完全不同的命运。活得最舒展的,是把自己变成基建、或者把息差自己留下来的那几家。这套“卖铲子”的逻辑甚至正在被复制到一个全新的商品上——算力:已经有人在做 GPU 的价格指数、聚合采购和计量计费(被戏称为“GPU 版的 Stripe”),芝加哥商品交易所(CME)甚至在跟它们合建算力期货,连贝莱德 CEO Larry Fink 都断言“会出现一个新资产类别:买算力期货”。每一个新商品诞生,都需要一整套卖铲子的金融基建——而铺基建的人,往往比生产商品的人活得更久。

我总结下来就一句话:卖铲子的人赚的是软件的钱,不是金融的钱——这就是它能穿越周期的根本原因。 下面三个主角,是这条逻辑的三种形态。

二、Stripe:皇冠,以及一张看懂金融科技的框架表

Stripe 在公开市场上几乎不披露财务细节,但它的打法本身就是“卖铲子”的最佳教科书——它从不靠某一个爆款产品,靠的是一连串“把自己变成所有人底层”的动作:

- 用 Tempo(它和 Paradigm 合建的支付链)联合 SWIFT、渣打、ANZ,去改造跨境报文的底层标准;

- 收购 Bridge(稳定币)、Privy(钱包)、Metronome(按用量计费),把“AI 时代怎么收钱”这条新费池提前圈进来;

- 它的公司注册工具 Stripe Atlas,自 AI 兴起以来新注册公司数同比涨了 41%——等于握着创业潮的先行指标。

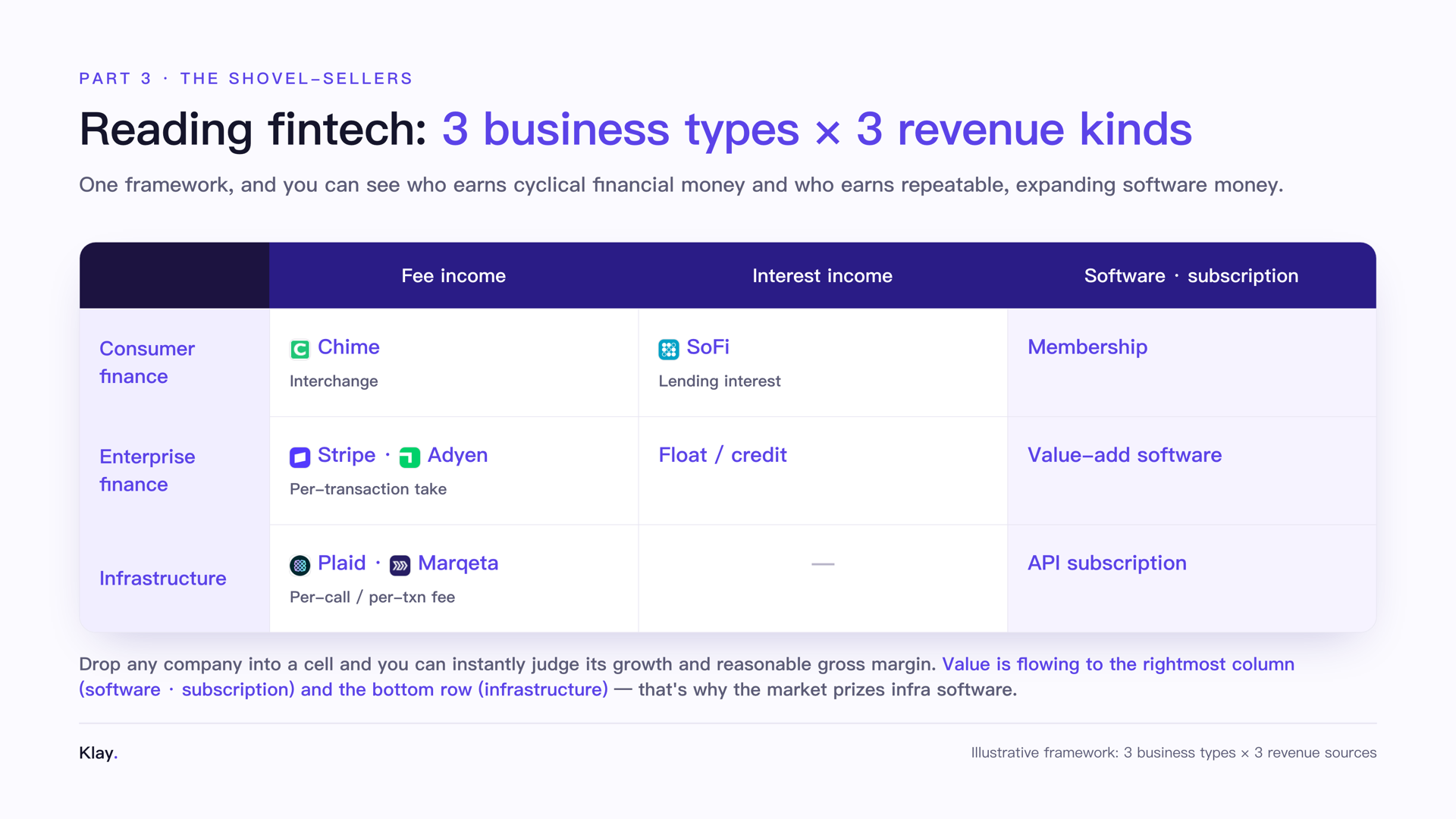

要把 Stripe 乃至整个赛道讲清楚,最好的办法是借一张框架表。金融科技公司其实可以用“三类业务 × 三种收入”来归类:

| 费用收入(手续费) | 利息收入 | 软件 / 订阅收入 | |

|---|---|---|---|

| 消费者金融(Chime、Klarna) | 刷卡交换费 | 放贷利息 | 会员订阅 |

| 企业金融(Stripe、Brex、Adyen) | 每笔支付抽成 | 浮存 / 信贷 | 增值软件 |

| 基础设施(Plaid、Marqeta) | 调用 / 笔费 | — | API 订阅 |

这张表的用处是:你把任何一家公司丢进格子里,立刻能判断它的增长性和合理毛利率。 消费者金融那一行,赚的是周期性的金融钱(第二篇讲过了,薄);而 Stripe 所在的“企业金融 + 基础设施”,越来越多的收入来自最右边那一列——可重复、会扩张、有软件经济学的钱。这就是市场愿意给它软件估值的原因。

顺着这张表最下面那行“基础设施”往下看,你会发现 Stripe 并不孤单,而是有一整批专门卖铲子的公司,每一家都死死卡住了一个别人绕不开的环节:

- Wise 卡住跨境——2026 财年收入 16.1 亿英镑(underlying income)、税前利润率 26%、服务约 1890 万跨境客户,把抽成压到 52 个基点还能维持这份利润,2026 年 5 月赴纳斯达克双重上市(主上市地仍在伦敦)、市值约 120 亿美元。它面对的不是一个市场,而是“一堆利基的集合”。

- Plaid 卡住数据——它是连接你的银行账户和各种金融 App 的“数据接口”,2026 年最新一轮估值约 80 亿美元(大白话:你可以把它理解成金融数据的“水电接口”,没有它,很多 App 连不上你的账户)。

- Marqeta 卡住发卡——年收入约 6.25 亿美元,专门把“发卡的能力”打包成 API,让任何一个 App 几行代码就能发出自己的卡;做“一键换卡”的 Knot,每月调用量已经冲到 1 亿次。

它们都不直接面向消费者,却让消费者用的每一个金融 App 都得从它们身上经过。这就是卖铲子最理想的位置:你不必赢得用户,你只要成为所有人的必经之路。

(大白话:take rate=抽成率,商家每做成 100 块交易,支付公司能拿走几毛几分。Stripe 名义费率约 2.9%,但其中大头要分给发卡行和卡组织,真正归自己的“净抽成”只是薄薄一层——所以支付是个“薄利多销、靠规模和软件加成”的生意。)

中国对标:很多人会拿支付宝、微信支付去对标 Stripe,这是误读。支付宝和微信是面向消费者的钱包入口(C 端);Stripe 是面向开发者和企业的收单基建(B 端)——几行代码,就能让任何一个网站收全球的钱。一个是水龙头,一个是水管。这个区别,正是第四篇的核心。

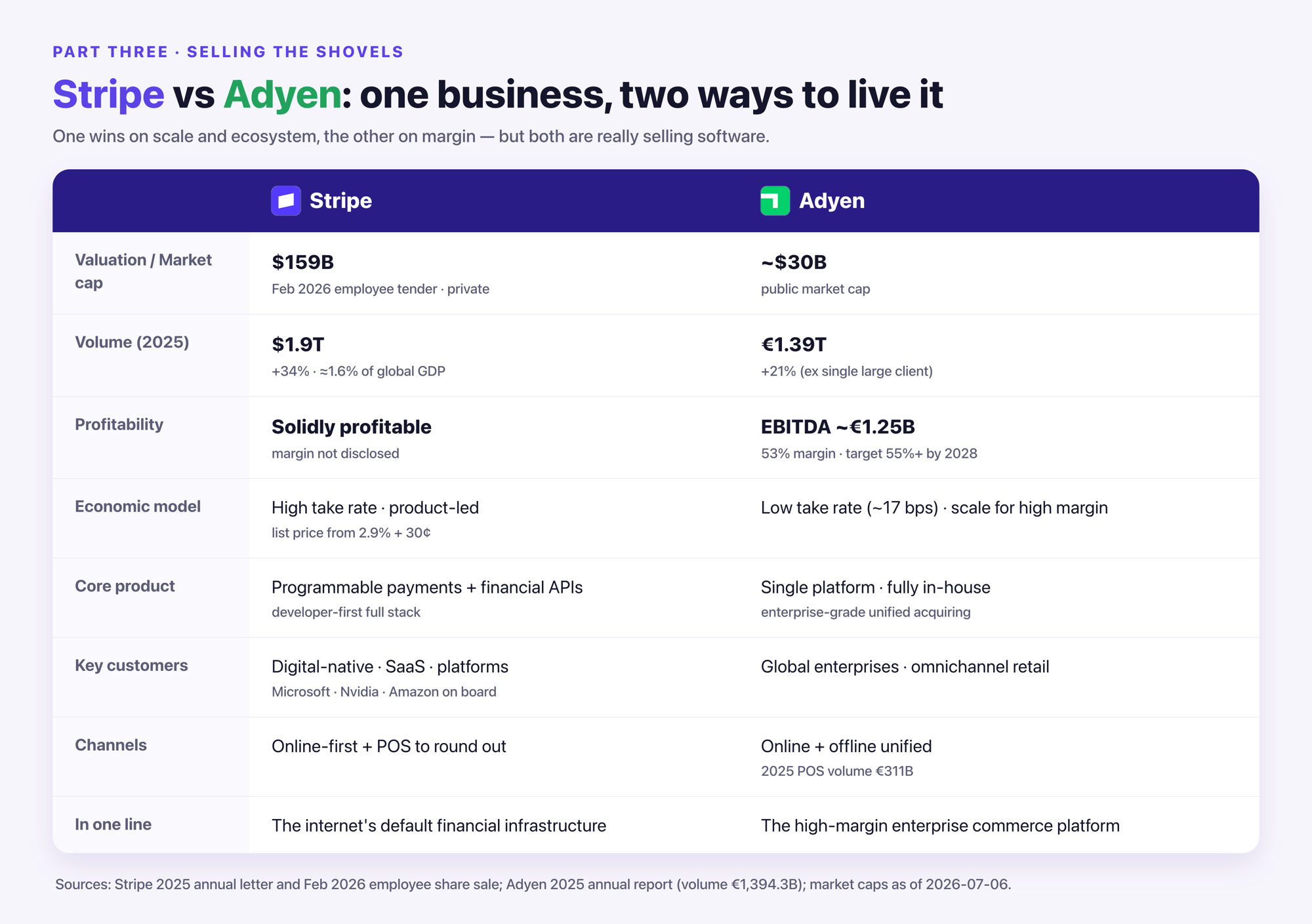

三、Adyen:盈利的标杆,Stripe 的一面镜子

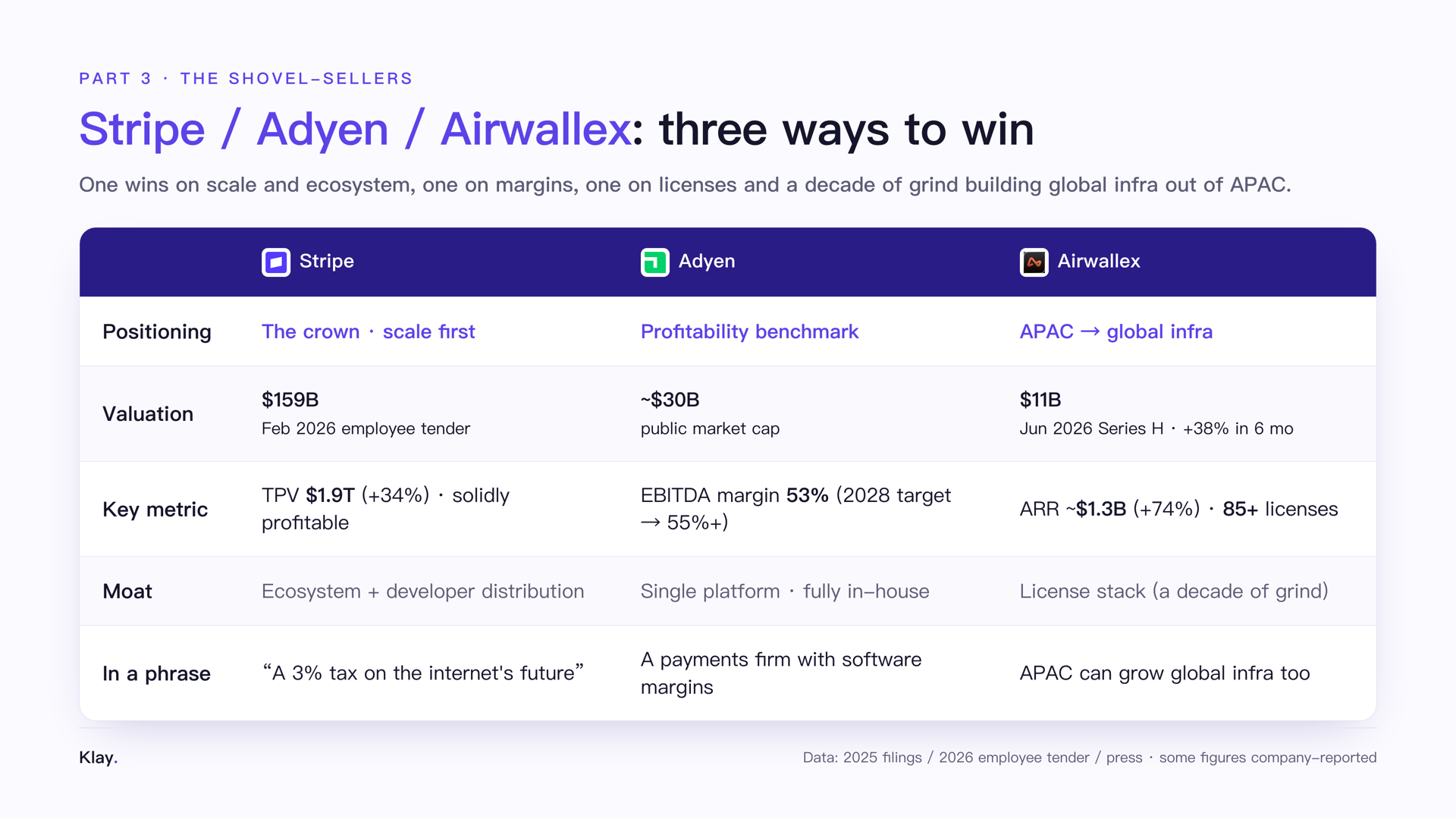

如果说 Stripe 代表“规模优先”,那荷兰的 Adyen 就代表“盈利优先”——它是这条赛道里最好的一把盈利标尺。

Adyen 2025 全年净收入 23.6 亿欧元、同比增长 21%(固定汇率),EBITDA 利润率高达 53%(2024 年是 50%),下半年单看更是冲到 55%,公司目标 2028 年稳定在 55% 以上。这是软件公司级别的利润率,不是金融公司的。

它凭什么能这么赚钱?因为它走的是“单一平台 + 全部自研”的路线:一套系统打通收单、风控、结算,不收购、不拼接、不靠外部处理商。代价是增长不如 Stripe 性感,好处是每一分收入的利润率都极高。它的抽成率(take rate)大约只有 17 个基点——每做成 1 万块交易只抽 17 块——靠的纯粹是天文数字般的交易量和极致的成本控制。

常被拿来对比两家的一个指标是“人效”(平均每个员工创造多少交易量):几年前 Stripe 高速扩张、员工冲到八千多人时,人效一度只有 Adyen 的四成左右——这正是当年市场唱衰它的论据之一。但 Stripe 后来用规模和盈利证明了:烧人扩张换来的生态卡位,本身就是一种护城河。所以这不是“谁对谁错”,是两条都能赢的路——只要你卖的是软件的钱。

把 Stripe 和 Adyen 摆一块,就是“卖铲子”这门生意的两种活法:一个用规模和生态卡位(Stripe 1590 亿估值、稳健盈利),一个用利润率封神(Adyen 53% margin、约 300 亿美元市值)。 但它俩指向同一个结论——支付基建是一门能做到软件级毛利、且赢家通吃的生意。

顺带说一句,Adyen 自己也曾在 2023 年被市场错杀过一次(股价单日暴跌),理由跟当年唱衰 Stripe 一模一样:“增长放缓了”。结果呢?两年后它的利润率不降反升。卖铲子的人,最经得起周期的拷问。

四、Airwallex:亚太也能长出全球基建,但代价是十年和八十五张牌照

第三个主角,离中国读者最近,也最适合过渡到第四篇——Airwallex(空中云汇),一家华人创立、总部现设新加坡与旧金山(发源于墨尔本)的跨境支付基建公司。

它的成绩单很硬:2026 年 6 月 Series H 估值 110 亿美元(半年内从 80 亿——2025 年底那轮——涨约 38%),年化收入约 13 亿美元、同比增长 74%,据其披露服务约 67.6 万家企业,并正全力扑向“agentic commerce”——给 AI agent 用的端到端财务平台。这其实是一个全新的、还没被牌照核心保护得那么死的品类:当 AI agent 开始替人下单、付钱、管钱,它们需要一层可编程的金融轨道;谁先做出“给 agent 调用的那层支付与托管接口”,谁就可能是 agentic 时代的 Stripe。

(大白话/对标:Airwallex 做的事,类似国内的连连、PingPong——帮企业跨境收款、付款、换汇——但它把战场铺到了全球,做的是“给企业用的跨境资金管道”。)

但 Airwallex 真正的护城河,藏在一个不性感的数字里:截至 2026 年中,它持有超过 85 张金融牌照/许可,覆盖近 200 个国家和地区。 这就是这门生意“一体两面”的本质——

牌照栈既是壁垒,也是账单。 它累计融资已达 18 亿美元、耗时约十年,才一张一张把这些牌照磨下来;正因为难,后来者也得同样烧十年的钱、走一遍同样的监管苦工,这才构成了别人抄不走的护城河。一句话:这门生意是用资本和时间堆出来的,不是用代码。

Airwallex 身上还压着两个一定要写进文章、且直通第四篇的细节:

第一,它正在把员工和数据迁出中国——公司明确表示美国客户的数据只存在美国或新加坡,中国团队无法访问。第二,它正面对“中国后门”的质疑:Khosla Ventures 的合伙人 Keith Rabois 公开指控它的中国工程团队和中国投资人(腾讯、红杉中国)使其在中国国安法下“可能有义务交出客户数据”;美国参议员 Tom Cotton 已要求调查。

这两件事合在一起,恰恰是这个系列最锋利的一处伏笔:一家带着中国基因的全球基建公司,能长到 110 亿美元,但它最成功的部分,是把总部、数据和增长都放在了中国之外;甚至要主动跟“中国”这两个字保持距离。这是偶然吗?第四篇会回答。

五、稳定币:卖铲子逻辑的完美复用——发币的是挖矿,铺渠道的才是卖铲子

三年前那批素材里,稳定币几乎不存在。但 2026 年,它成了“卖铲子”故事里增长最猛的新轨道——而且它完美复用了本篇的主框架。

先看格局的剧变:2025 年美国通过了 GENIUS 法案,第一次给稳定币发行方建立了联邦监管框架;稳定币龙头 Circle 已经上市。

但 Circle 的故事,恰恰是“发币不如卖铲子”的最佳反面教材。它上市后股价从 298 美元的高点一路回落到 60–70 美元、市值跌至约 160 亿。为什么这么脆?因为它 约 96%–99% 的收入来自储备金的利息——你把 1 美元换成 1 枚 USDC,Circle 拿着这 1 美元去买美国国债吃利息,一分都不分给你。

(大白话:稳定币≈“美元的随身碟”,把美元从银行账户拷出来、24 小时全球可带走;而发行方的本质,是一家“披着加密外衣的货币基金”——它的命脉,是美债利息和利率周期。)

所以稳定币这条新轨道上,真正在重演“卖铲子 vs 淘金”的分野:发币的 Circle 是在挖矿——重资产、吃利率周期、还要把一半收益分给铺渠道的人;而真正卖铲子的,是把稳定币铺成支付轨道、握住分发渠道的人。

最懂这条逻辑的,恰恰是 Coinbase。它自己不发币(USDC 是 Circle 发的),但它死死握着分发渠道:USDC 留在 Coinbase 平台上,它能拿走 100% 的储备收益,放在别处也能分走 50%——光这一项,2025 年就给它带来约 13.5 亿美元收入。发币的累死累活吃着利率周期,握渠道的躺着抽成——这就是“挖矿 vs 卖铲子”在稳定币世界里的翻版。

而把稳定币真正铺成轨道的,是 Stripe、Visa、Mastercard:Stripe 花 11 亿买下 Bridge;Mastercard 上线跨主流链的全天候稳定币结算,还以最高 18 亿美元收购稳定币基建 BVNK;更劲爆的是,有消息称 Stripe、Visa、Mastercard 正联手要推一个稳定币平台,Coinbase 也可能加入。当三家支付霸主一起来铺这条轨道,意味着稳定币的“卖铲子”层,已经成了非占不可的战略要地。

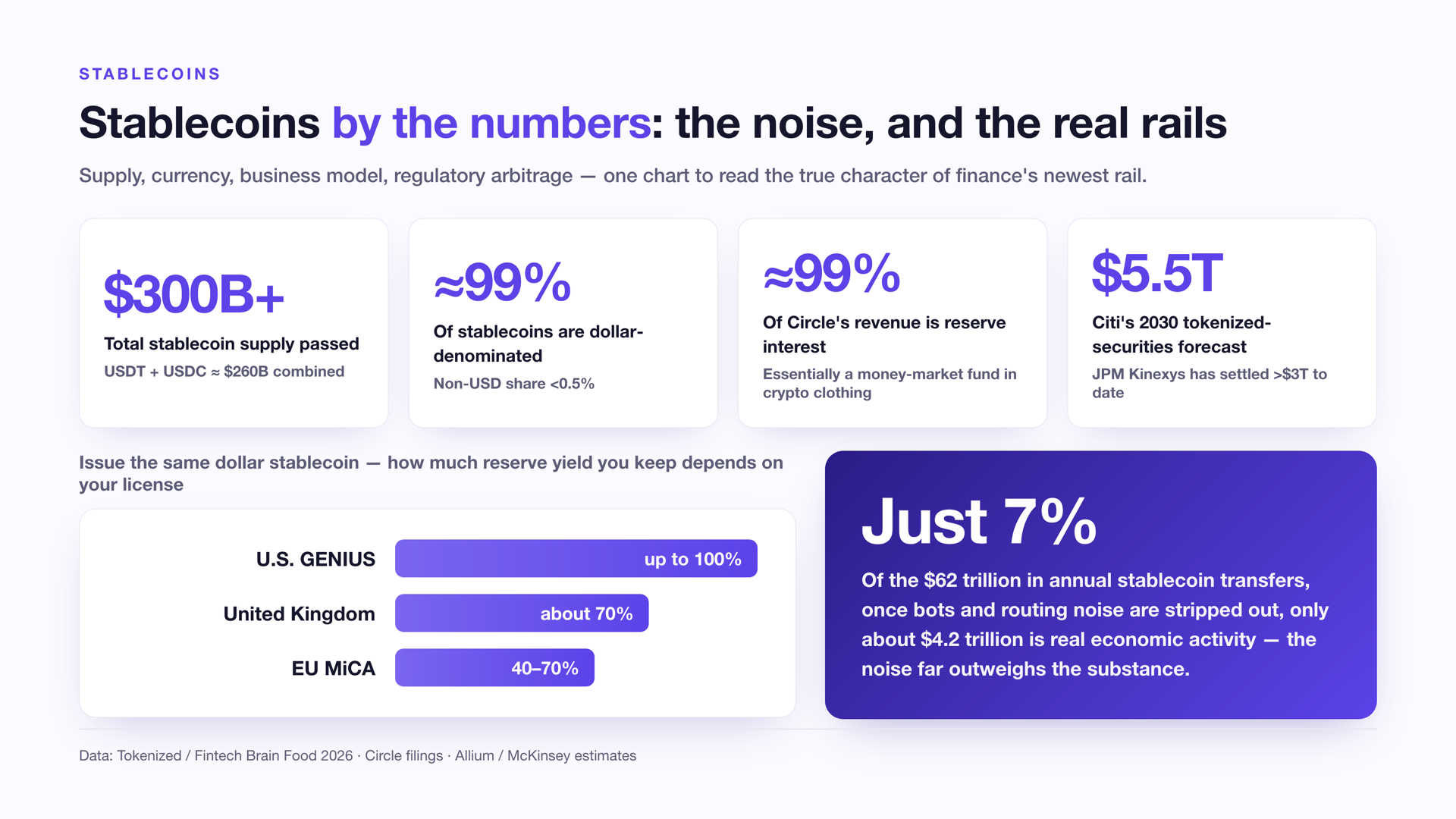

再往深一层,连银行和主权国家都开始亲自下场发币,但战场已经从“发行”转向“分销与互操作”:SoFi 成了首家向全体用户发稳定币的全国性持牌美国银行;七家大行共有的 Zelle 推出了 ZelleUSD,而最暴露动机的细节是——它选择先在印度上线、且偏偏不用稳定币(因为印度央行根本不承认稳定币);Tether 干脆替格鲁吉亚发了一枚国家稳定币,走的是“先帮你写规则、再受你委托发行”的主权客户模式。这背后是一条反复被验证的规律:业内已经放弃了“每家银行都发自己的币”的幻想——真正的战场从来不是发行,是分销、互操作,和把法币接进来的那些脏活。 有人把这层关系概括得很精准:稳定币是“轨道之上的轨道”(the rail above the rails)——一笔花旗的代币、一笔摩根大通的代币、一笔 Zelle 汇款、一条 SWIFT 报文,最后都要落到同一个公共层上。

而储备金这门“隐形息差”,本身就是一道分水岭:同样发美元稳定币,美国 GENIUS 框架下发行方最多能赚 100% 的储备收益,欧洲 MiCA 下只能赚 40%–70%,英国约 70%——规则的差异,直接决定了谁的生意更肥。 这也解释了为什么稳定币几乎是一场“美元的独家游戏”。

当然,新轨道也有翻车。代币化股票的第一次大规模压力测试就砸了:SpaceX 上市时,多家交易所临时取消“代币化 pre-IPO”并退款,超过 10 亿美元订单没成交,而且整个市场的底层路由竟然 100% 压在一家券商身上。深层障碍是美国的州法(UCC 第 8 条)还没适配代币化——“要走到真正的趋同,至少还要十年”。新轨道很性感,但铺轨道的脏活,依然是十年起步。

这条轨道还埋着第四篇的一颗大雷:全市场约 99% 的稳定币是美元。换句话说,稳定币越成功,越是在全球分发美元。一个靠资本管制守住货币主权的国家,要不要、能不能上这条轨道?这是“为什么中国出不了 Stripe”绕不开的一问。

六、Devil’s Advocate:基建会不会也被掀桌子?

按惯例,先把唱空的理由打满,再回到判断。

Bear case,认真地说:卖铲子的人也会被掀桌子。

第一,利率风险:稳定币这门最新的基建生意,Circle 有约 96%–99% 的收入吊在美债利息上——一旦进入降息周期,整个模型会从根上变形,这不是护城河,是顺风车。第二,监管与技术风险:代币化股票第一次大考就崩了(SpaceX、超 10 亿订单未成交、UCC 还要十年);加密的跨链桥按历史损失是全行业最差的品类,动辄几亿美元被盗。第三,也是最锋利的——商品化风险:连支付霸主的抽成率都在被往下压(Adyen 17 个基点、Wise 主动降到 52 个基点),那基建会不会最终沦为不赚钱的管道?

替反方说句大白话:铲子卖到最后,铲子本身也会变成白菜价——真正赚钱的也许是金矿,不是铲子厂。

但回到判断:赢家恰恰赢在“商品化不了”的那一层。

第一,基建留得住毛利,这是用脚投票投出来的——Adyen 守着 53% 的利润率、Stripe 三年从被唱衰翻盘到 1590 亿。第二,护城河根本不在“技术”,在分销、牌照、和那些“不性感的脏活”:Airwallex 的 85 张牌照、十年苦工,才是别人抄不走的东西。第三,市场已经用估值替这件事盖了章——上一篇那组数据值得再抄一遍:企业级基建的估值倍数平均 17 倍,而支付/转账只有 7.7 倍,最大的几笔 B2B 支付融资里,企业级基建拿走了 60%。当连卡组织自己都掏出几十亿美元来铺稳定币轨道时,恰恰说明这层基建是非占不可的战略高地。

七、收口:皇冠、新轨道,与一个绕不开的中国之问

三句话收束第三篇。

第一,企业支付基建是金融科技的皇冠。 因为它卖的是软件的钱、不是金融的钱——Stripe 1590 亿、Adyen 53% 利润率,市场用 17 倍对 7.7 倍的估值差,给“卖铲子”和“淘金”明明白白定了两种价。

第二,稳定币是这顶皇冠上新长出来的一条轨道。 但它依然遵循同一条铁律:发币的 Circle 在挖矿、吃利率周期;铺轨道的 Stripe、Visa、Mastercard 才是卖铲子的人。

第三,也是最重要的——卖铲子这门生意,是用资本、时间和牌照堆出来的。 Airwallex 用十年和八十五张牌照证明了“亚太也能长出全球基建”,但它同时也剧透了代价:要选对战场(跨境),要烧十年的钱,甚至要主动跟“中国”保持距离、还得回应“中国后门”的质疑。

那么问题来了:为什么这样一层“中立的、面向企业的、靠企业付费意愿和并购退出生态长大的基建”,在美国能长成皇冠,在中国却几乎长不出来?

这就是我们整个系列的终点——下一篇:《为什么中国出不了 Stripe》。

(本文数据采用 2026 年最新可得口径:Stripe 1590 亿美元估值与 1.9 万亿美元交易额来自其 2025 年度信及 2026 年 2 月员工股权交易;Adyen 净收入与 53% EBITDA 利润率来自 2025 全年股东信;Airwallex 估值、收入、牌照数来自公开媒体报道与公司披露,部分运营数据为公司口径;Circle 收入结构与股价来自其上市后公开披露;上市公司市值为 2026 年 6 月口径,会随交易日波动;稳定币与代币化相关动态综合自行业媒体与 fintech 研究者公开分享。)

"Why China Can't Produce a Stripe" series · Part Three

In brief — For every hundred dollars that flows across the internet, two or three are quietly skimmed off the top — and it isn't a bank doing the skimming. It's Stripe, Adyen, Airwallex: the people selling shovels. Last time I argued that most of the stars attacking the consumer side of banking have had a miserable run. This piece is about the winners: one that wins on scale and ecosystem lock-in, one that reaches godhood on margins, and one that spent a decade and eighty-five licenses laying global infrastructure across Asia-Pacific. And buried at the end is a fresh landmine: stablecoins, 99% of them pegged to the dollar.

Three years ago, the market handed Stripe a death sentence. The phrase it used was "death spiral."

In 2023, the company's internal valuation was beaten down from its 2021 peak of US$95 billion all the way to US$50 billion. The reporting called it a cash bonfire — growth stalling, "even US$50 billion looks expensive." Even its longtime bulls began to waver.

By February 2026, Stripe's latest employee share sale set the valuation at US$159 billion — up 74% from US$91.5 billion a year earlier. In 2025 it processed US$1.9 trillion in transaction volume, up 34% year on year, a figure equal to 1.6% of global GDP, and it was, explicitly, "solidly profitable." Even Microsoft routed "a substantial share" of its volume over to it, and the client roster added Nvidia and Amazon. It even wrote the largest check in its history — US$1.1 billion for the stablecoin company Bridge.

The bet that everyone dismissed as a "death spiral" paid off, three years on.

Which is the perfect footnote to the conclusion of the last piece: while most of the stars attacking the consumer side of banking are cut in half, halved again, or frozen out of the exit market, the people selling shovels are riding straight through the cycle.

This piece is about those shovel-sellers — why enterprise payment infrastructure is the crown of this whole race, what each of the three protagonists (Stripe, Adyen, Airwallex) stands for, and a track that barely existed in the source material three years ago but has since become a new battlefield: stablecoins. At the end I'll pose a question that carries the whole series to its finish: what makes the moat around this layer of shovel-selling infrastructure so deep? And why does almost none of it grow in China?

I'll use the freshest 2026 figures wherever I can. Let's begin.

I. Why Infrastructure Is the Crown: Shovel-Sellers Keep Their Margins

Let me plant the overall thesis first, then nail it down with the deals.

In every gold rush, the surest business was never digging for gold — it was selling shovels. For one reason only: infrastructure keeps the margin on its own layer, and shares it with no one.

This holds well beyond finance — AI right now is the same play. Through 2024 and 2025, the one quietly minting money wasn't any large model; it was Nvidia, selling shovels. Today the shovel has been handed one rung further upstream, to the memory-makers — Micron, SanDisk, SK Hynix, Samsung. In the bill of materials for a single AI chip, high-bandwidth memory (HBM) alone eats more than half, and Micron's 2026 capacity sold out long ago. The gold-diggers change with every wave; the shovel-sellers never stop counting cash.

The sharpest evidence is a valuation contrast — two fates on the same track. Both started in "corporate spend management" — issuing companies smart credit cards and automating expenses and cost controls along the way. The one that chose to become infrastructure, Ramp, is worth US$44 billion in 2026; the one that invented the category but chose to sell itself, Brex, was acquired by Capital One for US$5.15 billion. The former is 8.5 times the latter's exit price. The company that opened the category didn't earn the category's money — telling, isn't it.

Here's an analogy that makes it click: Stripe is to internet commerce what the water utility is to a city. Nobody gives the water company an innovation award, but every time the city turns on a tap, it's collecting. In its early days Stripe had an even wilder line for this — it wanted to become "a 3% tax on the future growth of the internet."

(In plain terms: embedded finance means slotting the functions that once belonged to banks — accounts, payments, lending — into any non-financial app, like Lego bricks. BaaS, banking-as-a-service, is the wholesale version: a licensed bank rents out its license and account capabilities for fintech companies to use.)

And AI is making this shovel-selling business more valuable still: it upgrades infrastructure from "helping people do things" to "doing things for them." One example is Lassie, which builds AI financial back-offices for doctors' practices and claims to automate 98% of bookkeeping — when infrastructure doesn't just save labor but does the whole job, what it can charge moves into an entirely different bracket.

The class of 2019 fintech stars has been completely reshuffled: Brex absorbed by Capital One, Ramp grown into US$44 billion of spend infrastructure, Mercury going out and getting a bank charter of its own — three companies that started on the same track, ending up in wholly different places. The ones living most comfortably are the few that turned themselves into infrastructure, or kept the spread for themselves. This shovel-selling logic is even being copied onto a brand-new commodity — compute: there are already companies building GPU price indices, aggregated procurement, and metered billing (dubbed "the Stripe of GPUs"), the Chicago Mercantile Exchange (CME) is co-building compute futures with them, and even BlackRock CEO Larry Fink has declared "there will be a new asset class: buying compute futures." Every time a new commodity is born, it needs an entire stack of shovel-selling financial infrastructure — and the people laying that infrastructure tend to outlive the people making the commodity.

I'll boil it all down to one line: shovel-sellers earn software money, not finance money — and that is the root of why they ride through cycles. The three protagonists below are three forms of that same logic.

II. Stripe: The Crown, and One Table for Reading All of Fintech

Stripe discloses almost no financial detail in public, but its playbook is itself the best textbook on selling shovels. It never leans on a single blockbuster product; it leans on a relentless series of moves to make itself the substrate underneath everyone:

- Using Tempo (the payments chain it co-built with Paradigm) to team up with SWIFT, Standard Chartered, and ANZ and rework the underlying standard for cross-border messaging;

- Acquiring Bridge (stablecoins), Privy (wallets), and Metronome (usage-based billing), fencing off the new fee pool of "how you get paid in the AI era" ahead of time;

- Its company-incorporation tool, Stripe Atlas, has seen new company registrations climb 41% year on year since the rise of AI — meaning it holds a leading indicator of the startup wave.

The best way to explain Stripe, and the whole race, is to borrow a table. Fintech companies can actually be sorted along "three business types × three revenue types":

| Fee revenue (transaction fees) | Interest revenue | Software / subscription revenue | |

|---|---|---|---|

| Consumer finance (Chime, Klarna) | Card interchange | Lending interest | Membership subscriptions |

| Enterprise finance (Stripe, Brex, Adyen) | A cut of each payment | Float / credit | Value-added software |

| Infrastructure (Plaid, Marqeta) | Per-call / per-transaction fees | — | API subscriptions |

The table's use is this: drop any company into a cell and you can immediately judge its growth potential and reasonable gross margin. The consumer-finance row earns cyclical finance money (covered in Part Two, and it's thin); Stripe's home turf — enterprise finance plus infrastructure — draws more and more of its revenue from the rightmost column: money that's repeatable, that scales, that has software economics. That's why the market is willing to hand it a software valuation.

Follow that bottom "infrastructure" row down and you'll find Stripe isn't alone — there's a whole cohort of dedicated shovel-sellers, each with a death grip on one link nobody can route around:

- Wise grips cross-border — FY2026 underlying income of £1.61 billion, a 26% pre-tax margin, serving roughly 18.9 million cross-border customers, holding that profit while squeezing its take down to 52 basis points; it dual-listed on Nasdaq in May 2026 (primary listing still in London) at a market cap of about US$12 billion. What it faces isn't one market but "a collection of niches."

- Plaid grips data — it's the "data interface" connecting your bank account to all manner of financial apps, valued at around US$8 billion in its latest 2026 round. (In plain terms: think of it as the plumbing socket for financial data; without it, many apps couldn't connect to your account at all.)

- Marqeta grips card issuance — roughly US$625 million in annual revenue, packaging "the ability to issue cards" into an API so any app can spin out its own card in a few lines of code; Knot, which does "one-click card switching," has pushed its monthly call volume to 100 million.

None of them face the consumer directly, yet every financial app a consumer touches has to pass through them. This is the ideal position for a shovel-seller: you don't have to win the users, you just have to become everyone's only way through.

(In plain terms: take rate is the cut — for every 100 dollars of transactions a merchant runs, how many cents the payments company keeps. Stripe's headline rate is around 2.9%, but most of that goes to the card-issuing bank and the card networks; the "net take" that's truly Stripe's own is only a thin sliver — which is why payments is a thin-margin, high-volume business that lives on scale and a software premium.)

The China comparison: many people reach for Alipay or WeChat Pay as the Stripe analog. That's a misreading. Alipay and WeChat are consumer-facing wallet gateways (the C-side); Stripe is developer- and enterprise-facing acquiring infrastructure (the B-side) — a few lines of code, and any website can collect money worldwide. One is the tap; the other is the pipe. That distinction is the core of Part Four.

III. Adyen: The Profitability Benchmark, Stripe's Mirror

If Stripe stands for "scale first," then the Netherlands' Adyen stands for "profit first" — it's the best profitability yardstick on this track.

Adyen's full-year 2025 net revenue was €2.36 billion, up 21% year on year (at constant currency), with an EBITDA margin as high as 53% (up from 50% in 2024), touching 55% in the second half alone, and the company targets a stable 55%-plus by 2028. These are software-company margins, not those of a financial company.

How does it make this much money? Because it runs a "single platform, all built in-house" model: one system spanning acquiring, risk, and settlement — no acquisitions, no bolt-ons, no reliance on outside processors. The cost is that growth isn't as sexy as Stripe's; the benefit is that every dollar of revenue carries an extremely high margin. Its take rate is only about 17 basis points — 17 dollars kept on every 10,000 dollars of transactions — riding purely on astronomical volume and ruthless cost control.

A metric often used to pit the two against each other is revenue-per-employee productivity (how much transaction volume each employee generates on average): a few years back, when Stripe was expanding at speed and its headcount blew past 8,000, its productivity dipped to roughly 40% of Adyen's — one of the market's arguments for writing it off at the time. But Stripe went on to prove, with scale and profit, that the ecosystem lock-in bought by burning through people is itself a kind of moat. So this isn't about who's right and who's wrong; these are two roads that both win — as long as what you're selling is software money.

Put Stripe and Adyen side by side and you have the two ways to live off selling shovels: one wins on scale and ecosystem lock-in (Stripe, US$159 billion valuation, solidly profitable), the other reaches godhood on margin (Adyen, 53% margin, roughly US$30 billion market cap). But both point to the same conclusion — payment infrastructure is a business that can hit software-grade margins, and it's winner-take-all.

Worth a footnote: Adyen too was once wrongly punished by the market, in 2023 (its shares crashed in a single day), for exactly the reason used to write off Stripe: "growth has slowed." And the result? Two years later its margin didn't fall — it rose. The shovel-seller stands up best to the cross-examination of the cycle.

IV. Airwallex: Asia-Pacific Can Grow Global Infrastructure Too — at the Cost of a Decade and Eighty-Five Licenses

The third protagonist is the closest to Chinese readers, and the best bridge into Part Four — Airwallex, a cross-border payment infrastructure company founded by ethnic Chinese entrepreneurs, now headquartered in Singapore and San Francisco (it began in Melbourne).

Its report card is solid: a Series H valuation of US$11 billion in June 2026 (up about 38% in six months from US$8 billion in its late-2025 round), annualized revenue of roughly US$1.3 billion, up 74% year on year, and — by its own disclosure — around 676,000 business customers served, while it throws itself fully at "agentic commerce": an end-to-end financial platform for AI agents to use. This is in fact a brand-new category, not yet locked down as tightly by license moats: when AI agents begin ordering, paying, and managing money on people's behalf, they need a layer of programmable financial rails; whoever first builds "the payment-and-custody interface that agents call" may become the Stripe of the agentic era.

(In plain terms / comparison: what Airwallex does resembles China's LianLian or PingPong — helping businesses collect, pay, and convert currency across borders — but it has spread the battlefield worldwide, building "cross-border money pipes for enterprises to use.")

But Airwallex's real moat hides in an unsexy number: as of mid-2026, it holds more than 85 financial licenses/permits, covering nearly 200 countries and regions. This is the two-sided nature of the business —

The license stack is both the barrier and the bill. It has raised US$1.8 billion in total and spent about ten years grinding these licenses out one at a time; and precisely because it's hard, latecomers must burn ten years of money too, walk the same regulatory drudgery, and only that constitutes a moat no one can copy. In a word: this business is stacked out of capital and time, not code.

Airwallex also carries two details that absolutely have to make it into this piece, and that lead straight into Part Four:

First, it is moving employees and data out of China — the company states plainly that U.S. customers' data lives only in the U.S. or Singapore, inaccessible to the China team. Second, it faces "China backdoor" scrutiny: Khosla Ventures partner Keith Rabois has publicly alleged that its China engineering team and Chinese investors (Tencent, Sequoia China) could leave it "potentially obligated to hand over customer data" under China's national security law; U.S. Senator Tom Cotton has already called for an investigation.

Put those two things together and you get the sharpest bit of foreshadowing in this whole series: a global infrastructure company with Chinese DNA can grow to US$11 billion, but its most successful parts are the ones that placed headquarters, data, and growth outside China — it even actively keeps its distance from the two characters "China." Is that a coincidence? Part Four answers.

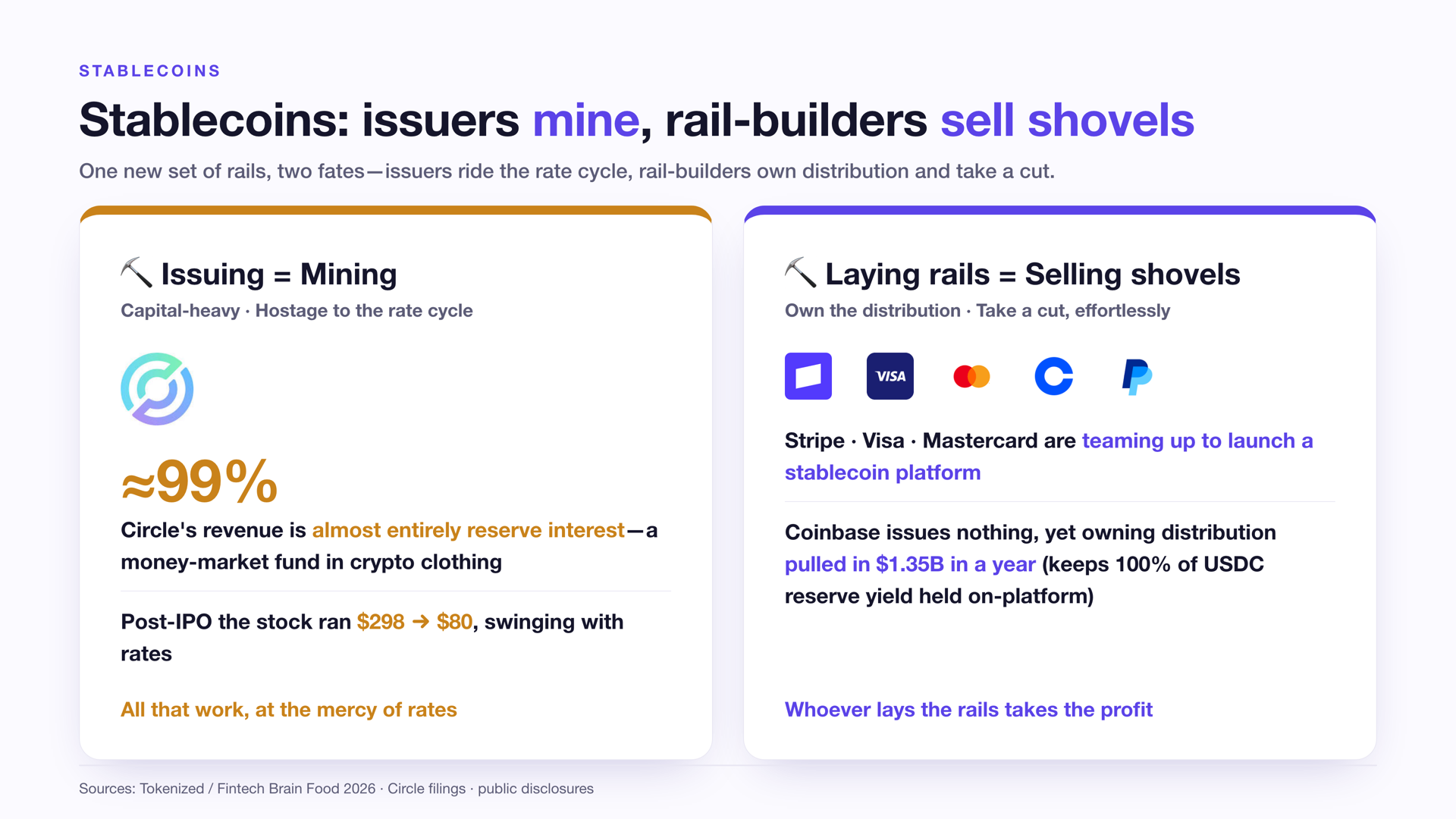

V. Stablecoins: A Flawless Reuse of the Shovel-Selling Logic — Issuing the Coin Is Mining, Laying the Rails Is Selling Shovels

In the source material three years ago, stablecoins barely existed. But in 2026 they've become the fastest-growing new track in the shovel-selling story — and they reuse this piece's master framework to perfection.

Start with the seismic shift in the landscape: in 2025 the U.S. passed the GENIUS Act, establishing a federal regulatory framework for stablecoin issuers for the first time; the stablecoin leader Circle is already public.

But Circle's story is exactly the best cautionary tale for "issuing the coin beats selling shovels — until it doesn't." After its IPO the stock slid from a high of US$298 all the way back to US$60–70, its market cap falling to roughly US$16 billion. Why so fragile? Because about 96%–99% of its revenue comes from interest on reserves — you convert US$1 into one USDC, Circle takes that dollar to buy U.S. Treasuries and pockets the interest, sharing not a cent with you.

(In plain terms: a stablecoin is roughly a "USB stick for dollars" — copy dollars out of your bank account and carry them anywhere in the world, 24 hours a day; and the issuer is, at heart, "a money-market fund in crypto clothing" — its lifeblood is Treasury yield and the interest-rate cycle.)

So on this new stablecoin track, the real "shovel-seller vs. gold-digger" split is playing out again: the issuer Circle is mining — capital-heavy, exposed to the rate cycle, and forced to share half its yield with the ones laying the rails; while the true shovel-sellers are the ones who turn stablecoins into payment rails and hold the distribution channels.

The one who understands this logic best is, of all companies, Coinbase. It issues no coin of its own (USDC is Circle's), yet it holds a death grip on distribution: USDC held on Coinbase's platform earns it 100% of the reserve yield, and 50% held elsewhere — that one line alone brought it roughly US$1.35 billion in revenue in 2025. The issuer works itself to death on the rate cycle; the channel-holder skims a cut lying down — that's the "mining vs. selling shovels" split, replayed in the stablecoin world.

And the ones truly turning stablecoins into rails are Stripe, Visa, and Mastercard: Stripe paid US$1.1 billion for Bridge; Mastercard launched round-the-clock stablecoin settlement across mainstream chains and acquired the stablecoin infrastructure firm BVNK for up to US$1.8 billion; and, more explosive still, there are reports that Stripe, Visa, and Mastercard are joining forces to launch a stablecoin platform, with Coinbase possibly joining too. When three payment titans come together to lay this rail, it means the shovel-selling layer of stablecoins has become strategic ground that must be seized.

Go one layer deeper and even banks and sovereign states are now issuing coins themselves, but the battlefield has shifted from "issuance" to "distribution and interoperability": SoFi became the first nationally licensed U.S. bank to issue a stablecoin to all its users; Zelle, jointly owned by seven big banks, launched ZelleUSD — and the most motive-exposing detail is that it chose to launch in India first, and pointedly not as a stablecoin (because India's central bank simply doesn't recognize stablecoins); Tether went ahead and issued a national stablecoin for Georgia, running a sovereign-client model of "write your rules for you first, then issue on your mandate." Behind all this is a rule that keeps being validated: the industry has abandoned the fantasy of "every bank issuing its own coin" — the real battlefield was never issuance; it's distribution, interoperability, and the dirty work of plugging fiat in. Someone captured the relationship precisely: stablecoins are "the rail above the rails" — a Citi token, a JPMorgan token, a Zelle transfer, a SWIFT message, all must ultimately land on the same public layer.

And that reserve business, the "invisible spread," is itself a watershed: for the same dollar stablecoin, an issuer can earn up to 100% of the reserve yield under the U.S. GENIUS framework, only 40%–70% under Europe's MiCA, and about 70% in the UK — the difference in the rules directly decides whose business is fatter. That also explains why stablecoins are almost entirely a "dollar-only game."

Of course, the new track has its wrecks too. Tokenized equities failed their first large-scale stress test: when SpaceX went public, several exchanges abruptly canceled "tokenized pre-IPO" offerings and issued refunds, more than US$1 billion in orders went unfilled, and the entire market's underlying routing turned out to rest 100% on a single broker. The deeper obstacle is that U.S. state law (UCC Article 8) hasn't yet adapted to tokenization — "getting to real convergence will take at least another ten years." The new track is sexy, but the dirty work of laying it still starts at a decade.

This track also buries a big landmine for Part Four: about 99% of all stablecoins are dollar-denominated. In other words, the more successful stablecoins become, the more they are distributing dollars globally. A country that defends its monetary sovereignty through capital controls — should it, and can it, board this track? That's an unavoidable question in "why China can't produce a Stripe."

VI. Devil's Advocate: Could Infrastructure Get Its Table Flipped Too?

As usual, let me max out the bear case before returning to the judgment.

The bear case, said in earnest: shovel-sellers can have their table flipped too.

First, rate risk: in stablecoins, the newest infrastructure business, Circle has roughly 96%–99% of its revenue hanging on Treasury interest — enter a rate-cutting cycle and the whole model warps from the ground up; that's not a moat, it's a tailwind. Second, regulatory and technical risk: tokenized equities crashed their first big exam (SpaceX, over US$1 billion in orders unfilled, UCC still a decade out); crypto's cross-chain bridges are, by historical losses, the worst category in the entire industry, with hundreds of millions of dollars stolen at a time. Third, and sharpest — commoditization risk: even the payment titans' take rates are being pressed down (Adyen at 17 basis points, Wise voluntarily cut to 52), so might infrastructure ultimately be reduced to unprofitable plumbing?

To make the other side's case in plain terms: sell shovels long enough and the shovels themselves become dirt cheap — the real money may be in the gold mine, not the shovel factory.

But back to the judgment: the winners win precisely on the layer that can't be commoditized.

First, infrastructure keeps its margin, and that's been voted on with real feet: Adyen holding a 53% margin, Stripe turning three years of being written off into US$159 billion. Second, the moat isn't in "technology" at all — it's in distribution, licenses, and the "unsexy dirty work": Airwallex's 85 licenses and decade of grind are the thing nobody can copy. Third, the market has already stamped this with valuation — that set of figures from the last piece is worth copying out again: enterprise-grade infrastructure trades at an average multiple of 17x, while payments/transfers get only 7.7x, and in the largest B2B-payment fundraises, enterprise-grade infrastructure took 60%. When even the card networks themselves are putting up billions to lay stablecoin rails, that only proves this infrastructure layer is strategic high ground that must be seized.

VII. Closing: The Crown, the New Track, and an Unavoidable China Question

Three sentences to close Part Three.

First, enterprise payment infrastructure is the crown of fintech. Because it sells software money, not finance money — Stripe at US$159 billion, Adyen at a 53% margin, with the market using a 17x-versus-7.7x valuation gap to price "selling shovels" and "digging for gold" as two plainly different things.

Second, stablecoins are a new track growing out of that crown. But they still obey the same iron law: the issuer Circle is mining, exposed to the rate cycle; Stripe, Visa, and Mastercard, laying the rails, are the ones selling shovels.

Third, and most important — the shovel-selling business is stacked out of capital, time, and licenses. Airwallex proved with a decade and eighty-five licenses that "Asia-Pacific can grow global infrastructure too," but it also spoiled the price: you have to pick the right battlefield (cross-border), burn ten years of money, and even actively keep your distance from "China" while fielding "China backdoor" scrutiny.

So here's the question: why does this layer — neutral, enterprise-facing infrastructure that grows on corporate willingness to pay and on an M&A exit ecosystem — grow into a crown in America, yet almost refuse to grow in China?

That's the finish line of the whole series — next up: "Why China Can't Produce a Stripe."

(The data in this piece uses the freshest figures available in 2026: Stripe's US$159 billion valuation and US$1.9 trillion in transaction volume come from its 2025 annual letter and its February 2026 employee share sale; Adyen's net revenue and 53% EBITDA margin come from its full-year 2025 shareholder letter; Airwallex's valuation, revenue, and license count come from public media reports and company disclosures, with some operating figures on a company basis; Circle's revenue structure and share price come from its post-IPO public disclosures; public-company market caps are on a June 2026 basis and will fluctuate with the trading day; stablecoin and tokenization developments are synthesized from industry media and public sharing by fintech researchers.)