硅谷Fintech观察②|为什么大家都去打银行:一张费池地图Silicon Valley Fintech Watch ② | Why Everyone Wants a Piece of the Banks: A Map of the Fee Pools

Translated from the Chinese original, first published on WeChat「世像」on July 11, 2026.本文 2026.07.11 首发于微信公众号「世像」。

「为什么中国出不了 Stripe」系列 · 第二篇

导读|银行不是一家公司,是一摞利润率天差地别的费池,叠在同一张牌照上——支付、刷卡费、放贷、净息差、跨境汇兑,每一块都肥到能单独养活一家上市公司。这十年美国 fintech 最凶的一波创业潮,几乎全涌向了这里。结果呢?冲在最前面的明星大多对折、腰斩,真正闷声赚到大钱的,是另一群人。这一篇,给你摊开一张费池地图。

先讲一个刚发生的事。

2026 年 5 月,一家叫 Parker 的美国 fintech,毫无预警地关了门。就在不久前,它还差点把自己卖掉——买家是做 AI 税务合规的 Avalara,这笔收购接近 9000 万美元;结果买家在最后一刻撤了。靠山一撤,账上的跑道瞬间归零。5 月 7 日,Parker 向特拉华破产法院提交了 Chapter 7。

Chapter 7 是什么?说白了就是美国的破产清算——不是重整、不是缓一缓喘口气,是公司直接关门、把资产变卖、清盘走人。

Parker 是家给中小企业做银行账户和信用卡的 fintech,对外一直说“融资超过 2 亿美元”。可这 2 亿里,有 1.25 亿其实是放贷额度——是拿来放贷的钱,不是自己的股本;与此同时,它的 CEO 还在对外说公司有 6500 万美元收入。数字很好看,公司却说没就没了。压垮它的不是没客户,是那笔本来谈好的收购最后一刻黄了——买家一撤,一切归零。

Parker 死在了“打银行”这条路上。但它不是孤例,它只是这门生意巨大引力场里的一个注脚。

上次我们聊到:美国券商和资管的“解耦”,是上一个十年的故事,而且早就基本干完了——佣金被 Robinhood 解耦,顾问费被智能投顾解耦,跑赢市场那个承诺被指数基金解耦,连“基金”这层壳都被 direct indexing 直接拆掉。一路拆到头,费率趋近于零。这条赛道上,你没法再去抢一只 0.03% 的标普基金,也没法在巨头免费送货、又垄断了规模利润的格局里,再造一家独立的大券商。

于是,一群最聪明的钱掉转枪口,齐刷刷地涌向了银行。

这一篇,我们聊两件事。第一,把“银行”这个庞然大物拆开,给你画一张费池地图——支付、刷卡费、放贷、净息差、跨境汇兑,每一块到底多大、谁在切、切得怎么样。第二,抛一个比“大家都在打银行”更反直觉的判断——打银行消费侧的那批明星公司,后来大多打得并不好;真正穿越了周期、闷声赚到大钱的,是另一群“卖铲子的人”。

数字尽量用 2026 年最新口径。往下看。

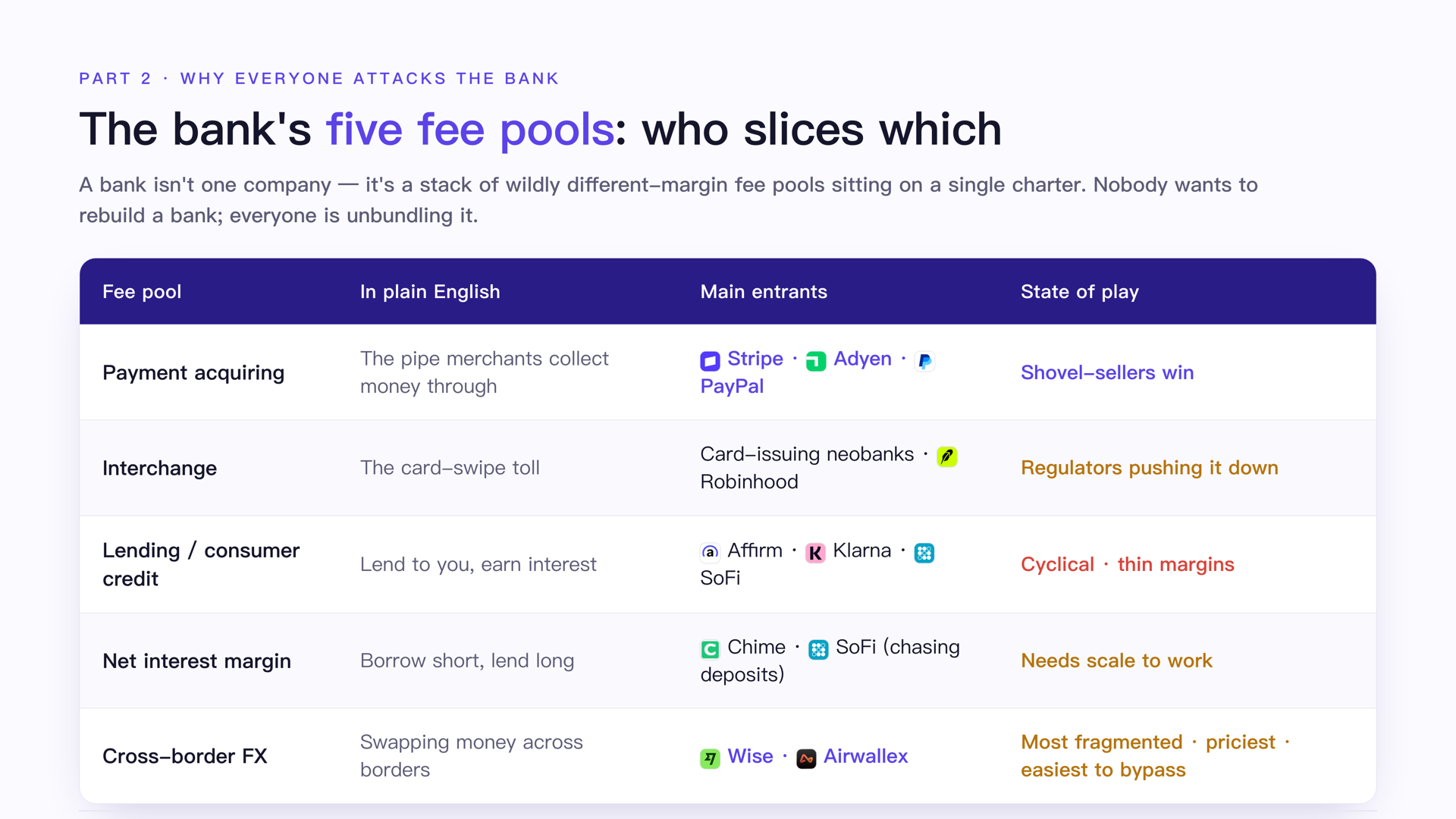

一、银行不是一家公司,是一摞费池

我们习惯把“银行”当成一个整体。但从 fintech 的视角看,银行其实是一摞彼此独立、利润率天差地别的费池,叠在同一张牌照上面:

- 支付收单——商家每收一笔钱,被抽一道手续费;

- 刷卡费(interchange)——你每刷一次卡,发卡行从中抽一笔“过路费”;

- 放贷与消费信贷——借钱给你、赚利息和手续费;

- 净息差(net interest margin)——用你的存款去放贷,赚“借短贷长”的利差;

- 跨境汇兑——帮你把钱从一个国家搬到另一个国家,赚汇差和手续费。

每一块都肥到足以养活一家上市公司,又彼此割裂到可以被单独切走。这就是“打银行”的玩家为什么这么多:他们根本不用攻下整座城,只要撬走其中一块砖。

打个比方你就懂了。如果说 SaaS 是把一套笨重的企业软件,拆成一个个能单独订阅的模块;那 fintech 干的,就是把一家银行,拆成一个个能单独收费的“功能键”。Stripe 撬走支付这个键、Wise 撬走跨境这个键、Affirm 和 SoFi 撬走借贷、Chime 撬走存款、Brex 和 Ramp 撬走公司卡——没人想从头造一家银行,所有人都在拆。

但在逐块看这张地图之前,先记住一句贯穿全篇的话:在银行这摞费池里,真正驱动增长的引擎,从来不是大家以为的“存款”,而是“支付”。 存款是“静止的钱”,趴在账上等着被放贷;支付是“流动的钱”,每流动一次就产生一次收费。摩根大通之所以是摩根大通,靠的是它每天清算超过 10 万亿美元的支付特许权,不是账上趴着多少存款。谁卡住了“钱的流动”,谁就握住了最肥、也最难被替代的那块费池。

下面这张地图,就是按“谁切了哪块、切得怎么样”画的。

| 费池 | 大白话 | 主要切入者 | 战况(剧透) |

|---|---|---|---|

| 支付收单 | 商家收钱的管道 | Stripe、Adyen、PayPal | 卖铲子的人,赢家 |

| 刷卡费 interchange | 刷卡的“过路费” | 各类发卡 neobank、Robinhood | 监管正在往下压 |

| 放贷 / 消费信贷 | 借钱给你赚利息 | Affirm、Klarna、SoFi | 周期性、薄毛利 |

| 净息差 | 借短贷长的利差 | Chime、SoFi(抢存款) | 需要规模才玩得动 |

| 跨境汇兑 | 跨境换钱 | Wise、Airwallex | 最碎、最贵、最易被绕开 |

二、刷卡费:最大的费池,正被监管从地基上撬动

先用大白话立住这个概念——它对中国读者最陌生,对美国却最要命。

刷卡费(interchange):你在美国每刷一次信用卡,商家被抽走一笔“过路费”,这笔费切成几块,最大一块归发卡银行——银行再拿这笔钱去补贴你的积分、返现、机场贵宾厅。美国高端信用卡那套“花得越多、返得越多”的飞轮,烧的就是这桶油。

2026 年,这块费池迎来了二十年来最重磅的一次震动:拖了二十年的商户诉讼,终于跟 Visa、Mastercard 达成和解,并在 6 月由法官 Brian Cogan 初步批准。

这里有个坑,写的人和读的人都极容易掉进去,必须先拎清楚:这其实是两个不同的和解。一个是赔历史损失的现金和解,基金规模 55.4 亿美元,赔给过去多付了手续费的商户;另一个是面向未来的降费和解,标价 380 亿美元——但这 380 亿不是一笔现金,而是“未来五年商户在刷卡费上累计能省下的钱”。后者的条款才是真正动地基的:信用卡刷卡费率五年内下调 10 个基点,标准消费卡费率八年内封顶在 1.25%,而且头一回允许商户按卡的档次选择性拒收那些最贵的高端卡。

听起来,高端卡飞轮的地基被撬松了。可真正有意思的是接下来的反转——飞轮并不会塌。

为什么?因为商户根本不敢在收银台赶走自己最好的客户。在美国,接近九成的信用卡消费都发生在带奖励的卡上,这恰恰是卡组织敢让步的底气:它赌的就是没有哪个商家会为了省那一点手续费,把刷着顶配卡、消费力最强的那群人拒之门外。更隐蔽的一层是,监管费尽力气压下来的那 10 个基点,很可能根本到不了商户手里——在 Square、Stripe 这类“打包定价”的模式下,省下的价差被支付处理商悄悄赚走,只有用“成本加成”定价的大商户才真占到便宜。被各方游说反复“代表”的小商户,反而是这场和解里沉默的输家。

其实这套“双边市场”的逻辑,早在 2018 年就被美国最高法院盖过章。当年俄亥俄等一批州政府联手告美国运通(Ohio v. American Express),说它那套“不许商户引导顾客改用低费率卡”的规矩涉嫌垄断、把商户手续费抬得太高。最高法院最后 5:4 判运通没违规,理由正是:刷卡是门“双边生意”——一头是商户、一头是持卡人,你不能只盯着商户被多收的那道手续费,还得看这笔钱在另一头补贴了多少持卡人的返现和权益。说白了,法院等于承认了“从商户抽水、拿去补贴持卡人”这套双边网络效应本身是合法的、甚至是有效率的。 所以监管今天想从费率上撬这块地基,撬的是一个连最高法院都背过书的模式——费劲,是有道理的。

再看中国这边:这套飞轮,在中国基本不存在。中国的刷卡费率被监管压得极低,又被支付宝和微信支付的二维码几乎完全绕开——这两家合计占了中国移动支付的九成以上。当支付的入口被两个二维码接管,“发卡行抽过路费、再拿过路费补贴积分”的整个链条就没了土壤。这就是为什么 interchange 这个词,对美国人天经地义,对中国人却近乎陌生——我们这一代人,几乎是直接跳过了信用卡的黄金时代。

三、放贷、净息差、跨境:被周期和摩擦定义的三块费池

先说放贷与消费信贷。媒体上喊得最响的数字,是美国人背着 1.25 万亿美元的信用卡账单还不上——这当然是个好标题。但有个反直觉的事实得先摆出来:信用卡其实只占美国人欠款总额的 6.6%,真正的大头是房贷,占了 70%。换句话说,“信用卡债务危机”在叙事里很吓人,在资产负债表上却只是个配角。

来切这块费池的新玩家,是“先买后付”(BNPL)。

BNPL 是啥?就是结账页面上那个“分 4 期、零利息”的按钮,本质是把一笔消费拆成几期的短期信贷——你把它理解成花呗、各种分期的美国版就行。

Affirm 和 Klarna 是这条赛道的代表。但你得记住这门生意的底色:它本质是放贷,吃的是信用周期的饭。 Klarna 2021 年还亏着约 7 亿美元、坏账约 5 亿(46 亿瑞典克朗);它的估值也正是从那一年的 456 亿,一路跌到 2025 年上市时的 150 亿。放贷可以增长得很快,但它从来不是一门能轻松穿越周期的生意——这一点,第四节还会反复出现。

说个中国人更熟的角色:滴滴。在拉美,滴滴早就不只是个打车的了,它把整套 fintech 铺成了全产业链——在墨西哥放贷(DiDi Préstamos,累计放款超 2000 万笔,其中约七成用户此前从没借过一分钱)、发信用卡(DiDi Card,墨西哥是它全球第一个发卡市场,一年就破了百万张),还上了 BNPL(叫 DiDi Paga Después,就是“先买后付、分期还”);在巴西,它旗下的 99Pay 干脆直接接进了本地的即时支付系统 PIX。一个打车起家的公司,跑到异国他乡把放贷、发卡、先买后付、支付一条龙全做了——这恰恰说明 BNPL 从来不是一门能单独立着的生意,它只是全套消费金融里的一环。

再看净息差,大白话就是银行“借短贷长”赚的那个利差——给存款人低息、向借款人收高息,中间的差就是这块费池。它的特点是强周期:2026 年一季度,美国全行业的净息差环比下滑了 8 个基点到 3.31%,而同期行业净利润其实还在涨、达到 805 亿美元。利润在涨、息差在缩,这种背离本身就是周期的指纹——靠净息差吃饭的生意,命脉攥在利率手里,不在自己手里。有意思的是,这一年消费者信心调查跌到几十年来的谷底,但银行高管看到的实际消费和借贷却相当强劲——PNC 的 CEO 干脆说,他“没法把那些关于消费者信心的头条调查,跟我们业务里每天看到的东西对上号,几乎完全相悖”。费池的真实温度,藏在交易数据里,不在问卷里。

再看地图上最碎、也最贵的一块:跨境汇兑。

这块费池为什么贵,得用大白话讲清楚(因为它正是下一篇“卖铲子的人”要绕开的痛点):一家中小银行没资格直接接入别国的清算系统,只能在大银行那里开一个“代理行账户”(correspondent account)——于是每笔电汇被收 5 到 50 美元的固定费、几百万美元的资金被迫闲置在不生息的海外账户里、一次系统误报还得再交 20 到 100 美元的“调查费”。再往上看,连 SWIFT 都常被冤枉:慢和贵的根源不在 SWIFT 这张网,而在银行和各国央行的截止时间。

正因为传统轨道的摩擦厚到离谱,专门来切这块肉的玩家活得很好。Wise(你把它理解成“把跨境汇款做得又便宜又透明”的玩家,类似国内做跨境收付的连连、PingPong 在个人和中小企业侧的角色)2026 财年收入 16.1 亿英镑(underlying income)、同比增长约 18%,服务约 1890 万跨境客户,把跨境抽成率一路降到 52 个基点还能保持 26% 的税前利润率——2026 年 5 月它还赴纳斯达克双重上市(主上市地仍在伦敦),市值约 120 亿美元。它的创始人当年建这家公司,就因为两个住在伦敦的人,一个拿英镑要还爱沙尼亚的房贷、一个拿克朗要付伦敦的生活费,受够了银行那道藏起来的汇率差。

四、反转:打银行消费侧的,大多很惨;卖铲子的,继续封神

现在到全篇的支点。把同一段时间窗里两类公司摊开摆一块,对比刺眼到几乎像一则寓言。

先看消费侧——那些直接面向你我、要“重做一家银行”的明星公司。

它们的增长数字往往很漂亮,可只要往单位经济和估值里瞟一眼,故事就变了:

- Chime,美国 neobank 的标杆,2025 年 6 月上市,发行市值约 116 亿美元——听着不小,可这已经比它 2021 年私募市场上 250 亿美元的峰值打了对折还多;上市后股价继续回落,一度只剩 66 亿上下、如今回到约 80 亿。它确实在 2026 年一季度做到了上市后首次 GAAP 盈利、收入增长 25%,但市场依然只肯给它很低的估值——等于把“消费侧薄毛利、强周期”这件事,直接写进了价签。

- Klarna,欧洲“先买后付”(BNPL,大白话就是花呗式的分期消费)的代表,估值从 2021 年的 456 亿美元,一路跌到 2025 年 9 月上市时的约 150 亿——三分之二的价值在四年里蒸发了。

- 更冷的是退出的价码。门不是没开——Chime、Klarna 都上了市——但都是按腰斩再腰斩的价格挤出去的。据 CB Insights,2026 年一季度全球 fintech 并购只有 199 笔、连跌至六个季度新低;10 亿美元以上的大额退出,从上年同期的 14 笔掉到 6 笔。

- 单位经济更是触目惊心:一家持牌 neobank(Varo)账户数一年涨了约一半,摊到每个账户上的存款却只有 52 美元——几乎可以断定它的客户要么是月光族、要么只把它当个可有可无的副账户;而 Robinhood 那张“所有消费 3% 无限返现”的高端卡,单看刷卡本身几乎是负毛利——据 Flagship Advisory Partners 拆算,每个持卡人一年给它赚的不超过 140 美元(还主要是利息),真正回血靠的是会员费、被黏住的资产、和 Gold 用户一年付的 6.56 亿美元融资利息——说白了,这是一门“赔本赚吆喝”的生意,返现是诱饵,钱在别处赚。

把消费侧的整张牌桌摆出来看会更清楚:Chime 约 80 亿、SoFi 约 222 亿、Affirm 约 260 亿、Block(Cash App 的母公司)约 443 亿美元——除了 Robinhood 因为加密和预测市场的狂热被炒到约 1015 亿(这本身就是周期的信号),其余大多低于各自私募时期的高峰,或远远够不到头部基建。

(对标一下:这些 neobank = 纯数字银行,没有网点、靠一个 App 获客和发薪日提前到账这类小功能黏住用户,国内最接近的是微众银行、网商银行的 C 端零售版。)

这一桌人共同的处境是:增长靠烧钱买来,利润靠交叉补贴撑着,估值随市场情绪起落。

再看卖铲子的一侧——那些不直接面向消费者、而是给所有人提供支付基建的公司。

同一段时间里,它们在封神:

- Stripe 是最戏剧性的反转。2023 年,拾象那篇报道里它还被唱衰成“死亡螺旋”,内部估值一度被打到 500 亿美元都嫌贵;到 2026 年 2 月,它最新一轮员工股权交易把估值定在了 1590 亿美元,比一年前的 915 亿涨了 74%。2025 年它处理了 1.9 万亿美元的交易额、同比增长 34%,相当于全球 GDP 的 1.6%,而且“稳健盈利”;连微软都把“相当一部分”交易量切给了它,客户名单上还站着英伟达、亚马逊。它还掏出史上最大一笔收购——11 亿美元买下稳定币公司 Bridge。当年那个“否极泰来”的赌注,赌赢了。

- Adyen,欧洲的支付收单巨头,2025 全年净收入 23.6 亿欧元、同比增长 21%(固定汇率),EBITDA 利润率高达 53%,目标 2028 年做到 55% 以上——这是软件公司级别的利润率,不是金融公司该有的。

- 有一个对照特别扎眼(下一篇还会细讲):同样从“企业支出”这个赛道起家,选择做基建的 Ramp 估值 440 亿美元,而开创了这个品类、却选择被收编的 Brex,2026 年被 Capital One 以 51.5 亿美元收购——前者是后者退出价的 8.5 倍。

其实开头那家倒掉的 Parker,背后是一整条 SMB(中小企业)银行的战线,而这条线上的命运分野,比消费侧还要刺眼。同样是给中小企业做账户和公司卡:Parker 直接清盘出局;开创了这个品类的 Brex,2026 年初被 Capital One 以 51.5 亿美元收编、成了大银行的一部分;Mercury 走的是第三条路——它在 2025 年底干脆去申请自己的银行牌照,想从“借别人的银行牌照”变成“自己就是银行”,如今客户超 30 万、2025 年处理了 2480 亿美元交易额。

最有意思的是 Slash:它最早是给“球鞋倒爷”发卡的(这群人流水很大,却因为年纪小、没注册公司,连张像样的银行卡都办不下来),结果 Kanye West 一番反犹言论把整个球鞋市场干崩,Slash 收入一夜蒸发八成;两个刚辍学的创始人硬是掉头转向,改去给营销代理、加密公司、甚至空调安装商这些细分行业做垂直银行,2025 年做到 2.5 亿美元年化收入,2026 年 4 月融了 1 亿、估值冲到 14 亿美元。你看,同一条 SMB 银行的赛道上:有人清盘、有人被大行收编、有人干脆自己去变成银行、有人靠一次转身求生——能“闷声活下来、甚至活得好”的,要么把自己嫁进大银行,要么找到一个极窄、极深、别人懒得碰的垂直行业。

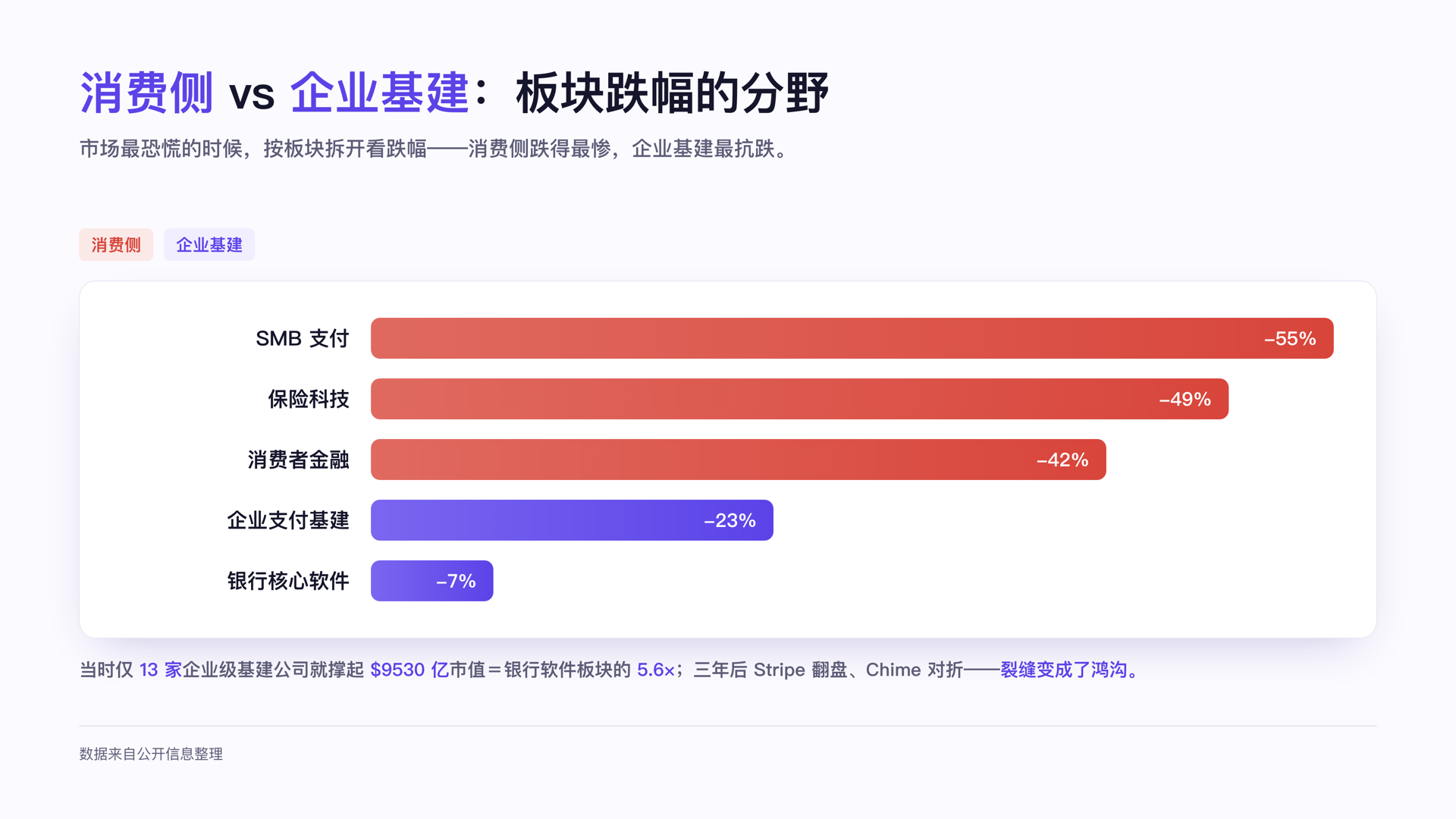

其实早在 2022 年市场最恐慌的时候,这条裂缝就已经被画得清清楚楚。当年 Coatue 把上市的 fintech 公司按板块拆开看跌幅:消费侧的中小企业支付跌了 55%、保险科技跌了 49%、消费者金融跌了 42%;而企业支付基建只跌了 23%、银行核心软件只跌了 7%——当时光是 13 家企业级基建公司,就撑起了 9530 亿美元市值,是整个银行软件板块的 5.6 倍。三年过去,这个结构非但没反转,反而被现实验证得更彻底:那一边 Chime 上市对折、Klarna 腰斩,这一边 Stripe 从被唱衰一路翻盘到 1590 亿。裂缝没有愈合,它变成了鸿沟。

这两侧的命运分野不是偶然,是被市场用一套清清楚楚的估值逻辑定了价。一份 2026 年一季度的统计说得很直白:企业级基建类 fintech 的估值倍数平均 17 倍、最高的一档;而支付/转账类只有 7.7 倍。为什么?因为前者有“软件经济学”(收入可重复、客户还会扩张),后者的增长要靠堆更多交易量、扛更多风险和成本,所以市场按“软件”给基建估值、按“金融服务”给支付和消费估值。同期另一组数据佐证了同一方向:最大的几笔 B2B 支付融资里,企业级基建拿走了 60%。

这正是上一篇那把钥匙的延续:在这个行业,估值跟的从来不是你“经手”了多少钱,而是你能从里面“赚到”多少、以及用什么倍数被定价。 经手万亿、却把费率打到零的消费侧,远不如经手交易、却能榨出软件级毛利的基建侧值钱。

五、抬个杠:可消费侧真的“很惨”吗?也许该打的就是它

按惯例,这一节我认真替反方说话——先把唱多消费侧的理由打满,再回到我的判断。

Bull case,认真地说:打银行消费侧,故事其实很硬。

第一,它真的能盈利。Chime 上市后已经做到 GAAP 盈利、收入增长 25%、会员超过 1000 万。第二,它有全世界最强的反例——Nubank:这家巴西数字银行如今市值约 620 亿美元,用户超过 1.31 亿,覆盖了约 62% 的巴西成年人,是巴西最大的私营金融机构。它证明了纯数字银行可以长成吞掉传统大行的巨兽。第三,消费侧直达 C 端、自带分销,不像基建要看大客户脸色——Cash App 一上线稳定币,背后就是接近 6000 万的用户基数。第四,连“超级 App”的故事都讲得通:Robinhood 如今市值高达约 1015 亿美元,远超绝大多数消费 fintech,它正从“赌徒的狂欢”洗白成“年轻一代的财富入口”。第五,那个吓人的“存款大逃亡”也没发生——Coinbase 给稳定币持有人付了近三年 4% 以上的收益,说好的存款外流根本没出现,过去两年美国银行存款总额反而还在涨。

替反方补一句类比:巴西版的 Google 还是 Google,但巴西版的“摩根大通”是 Nubank——在新兴市场,本土的 C 端数字银行不是造不出,而是直接把原版拍在了沙滩上。所以押注消费侧,并不傻。

但回到我的判断:这套 bull case,撞上的是单位经济、估值倍数和退出环境这三堵墙。

先拆最性感的两个反例。Nubank 的成功,很大程度上是巴西的高利率红利,不是科技魔法——在一个基准利率动辄两位数的国家,光是吃存贷利差就足够养出一家巨兽;这套模型换到低利率的成熟市场,立刻失灵。Robinhood 的高市值同样脆弱:它的利润依然高度依赖交易、尤其是加密这种极端周期的品种,市场一冷、加密一跌,利润立马现原形;而它新押注的预测市场,头上还悬着“这到底是金融工具还是变相赌博”的监管利剑。

再看那三堵墙。单位经济——Varo 人均存款 52 美元、Robinhood Gold 卡每户一年赚不到 140 美元(Flagship 拆算),这种生意天生靠交叉补贴硬撑。估值倍数——市场只肯给消费侧“金融服务”的低倍数(7.7 倍),而把“软件”的高倍数(17 倍)留给基建。退出环境——Klarna 四年蒸发三分之二价值、Chime 上市即对折、10 亿美元以上的大额退出一年内从 14 笔掉到 6 笔,资本已经用脚投票。

而最能说明问题的,是消费侧赢家们自己的选择:Chime、SoFi、Mercury 都在拼命去拿银行牌照,因为只有变成银行,才能把分给合作行的息差自己留下;够不到这一步的“第二波 neobank”,则只能等着被超级 App 收编——这恰恰是我第四篇要讲的故事的开头。

六、收口:解耦之后,谁穿越了周期?

三句话收这第二篇。

第一,银行的费池又大又散,所以所有人都来打。 支付、刷卡费、放贷、净息差、跨境汇兑,每一块在美国都是十亿美元级别的楔子;旧体验最烂、可乘之机最多。这是过去十年最汹涌的一场创业潮。

第二,但打银行消费侧的那批明星公司,后来大多打得并不好。 Chime 上市即对折、Klarna 四年蒸发三分之二、大额退出一年内从 14 笔掉到 6 笔——它们大多是周期性、薄毛利、烧钱的生意,赢家的归宿要么是变成一家银行,要么是被超级 App 收编。

第三,真正穿越了周期、闷声赚到大钱的,是另一群“卖铲子的人”。 Stripe 三年从 500 亿被唱衰、翻盘到 1590 亿且稳健盈利,Adyen 守着 53% 的软件级利润率,市场用 17 倍对 7.7 倍的估值差,给“企业级基建”和“消费支付”明明白白地定了两种价。

那么,这群“卖铲子的人”到底是谁、它们的护城河凭什么这么深、稳定币这条新轨道又会怎么改写战局?

这就是我下一篇的事——《卖铲子的人:Stripe / Adyen / Airwallex》。

最后附赠一张美国人钱包的体检单——看懂它,就看懂 BNPL 和 neobank 的需求是从哪儿长出来的。

(本文数据采用 2026 年最新可得口径:Parker 于 2026 年 5 月 7 日提交 Chapter 7、拟收购方 Avalara 及约 9000 万美元收购、2 亿美元融资含 1.25 亿放贷额度等来自公开报道;Ohio v. American Express 为美国最高法院 2018 年 5:4 判决;DiDi 拉美放贷/发卡/BNPL 数据来自公开报道;Brex 被 Capital One 以 51.5 亿美元收购、Mercury 申请银行牌照与 2480 亿美元交易额、Slash 2.5 亿美元年化收入与 14 亿美元估值均为公开披露;Stripe 1590 亿美元估值与 1.9 万亿美元交易额来自其 2025 年度信及 2026 年 2 月员工股权交易;Adyen 数据来自 2025 全年股东信;Chime、Klarna 市值与 IPO 数据来自公开市场披露;Visa/Mastercard 两笔和解金额口径分别为 55.4 亿美元现金基金与 380 亿美元五年累计降费;上市公司市值为 2026 年 6 月口径,会随交易日波动;fintech 并购 199 笔与 $1B+ 退出 14→6 笔来自 CB Insights State of Fintech Q1 2026;Robinhood Gold 卡单位经济(140 美元/6.56 亿美元)来自 Flagship Advisory Partners 拆算。)

"Why China Has No Stripe" series · Part Two

In brief — A bank isn't one company. It's a stack of fee pools with wildly different margins, all riding on a single charter — payment acquiring, interchange, lending, net interest margin, cross-border FX. Each one is fat enough to sustain a listed company on its own. Over the past decade, the fiercest wave of American fintech startups poured almost entirely into this space. And the result? Most of the stars that charged hardest ended up cut in half, or worse. The ones who quietly made the real money were a different crowd. This piece lays out a map of the fee pools.

Let me start with something that just happened.

In May 2026, an American fintech called Parker shut down without warning. Not long before, it had nearly sold itself — the buyer was Avalara, which does AI tax-compliance, and the deal was worth close to US$90 million. Then, at the last moment, the buyer walked. With its backstop gone, the runway on its books vanished overnight. On May 7, Parker filed for Chapter 7 in the Delaware bankruptcy court.

What's Chapter 7? In plain terms, it's American bankruptcy liquidation — not a restructuring, not a chance to catch its breath, but the company simply closing its doors, selling off its assets, and winding up for good.

Parker was a fintech providing bank accounts and credit cards to small and mid-sized businesses, and it had long told the world it had "raised over US$200 million." But of that US$200 million, US$125 million was actually a lending facility — money to lend out, not the company's own equity. Meanwhile its CEO was still telling the world the company had US$65 million in revenue. The numbers looked great, yet the company was gone in a blink. What broke it wasn't a lack of customers; it was that the acquisition it had already lined up fell through at the eleventh hour — the buyer pulled out, and everything went to zero.

Parker died on the road to "taking on the banks." But it wasn't a one-off. It was just a footnote in the enormous gravitational field of this business.

Last time we covered how the "unbundling" of American brokerage and asset management was the story of the previous decade — and one that was largely finished long ago. Commissions were unbundled by Robinhood, advisory fees by robo-advisors, the promise of beating the market by index funds, and even the "fund" wrapper itself was pried apart by direct indexing. Unbundled all the way down, fees trended toward zero. On that track, you can no longer go after a 0.03% S&P fund, nor can you build another independent, large brokerage in a landscape where the giants ship for free and monopolize the scale profits.

So the smartest money swung its guns around and poured, in lockstep, toward the banks.

This piece covers two things. First, we'll take apart that behemoth called "the bank" and draw you a map of the fee pools — payment acquiring, interchange, lending, net interest margin, cross-border FX — how big each one really is, who's slicing into it, and how well they're doing. Second, we'll offer a judgment more counterintuitive than "everyone's taking on the banks": the star companies attacking the consumer side of banking mostly went on to do quite poorly; the ones who actually crossed the cycle and quietly made the big money were a different crowd — the "people selling shovels."

Numbers are drawn from the most recent 2026 figures wherever possible. Read on.

I. A Bank Isn't One Company — It's a Stack of Fee Pools

We're used to thinking of "the bank" as a single whole. But from a fintech vantage point, a bank is really a stack of mutually independent fee pools with wildly different margins, all riding on a single charter:

- Payment acquiring — every time a merchant collects money, a fee is skimmed off;

- Interchange — every time you swipe a card, the issuing bank skims a "toll";

- Lending and consumer credit — lending you money, earning interest and fees;

- Net interest margin — using your deposits to lend, earning the "borrow short, lend long" spread;

- Cross-border FX — moving your money from one country to another, earning the exchange spread and fees.

Each is fat enough to sustain a listed company, and each is severed enough from the others that it can be sliced off on its own. That's why there are so many players "taking on the banks": they don't need to conquer the whole city — just pry loose one of its bricks.

Here's an analogy that makes it click. If SaaS took one clunky enterprise software suite and broke it into modules you could subscribe to individually, then what fintech does is take a bank and break it into individual "function keys" that can each be billed separately. Stripe pried loose the payments key, Wise the cross-border key, Affirm and SoFi the lending key, Chime the deposits key, Brex and Ramp the corporate-card key — nobody wants to build a bank from scratch; everyone is taking one apart.

But before we walk this map pool by pool, hold on to one line that runs through the whole piece: within this stack of fee pools, the engine that truly drives growth has never been the "deposits" everyone assumes, but "payments." Deposits are "money at rest," sitting on the books waiting to be lent out; payments are "money in motion," and every time it moves, a fee is generated. JPMorgan is JPMorgan because of the payments franchise it clears — more than US$10 trillion a day — not because of how much deposit money is parked on its books. Whoever chokes the "flow of money" holds the fattest, and hardest-to-replace, pool of all.

The map below is drawn around "who sliced which pool, and how well they did it."

| Fee pool | In plain terms | Main entrants | The state of play (spoiler) |

|---|---|---|---|

| Payment acquiring | The pipe merchants collect through | Stripe, Adyen, PayPal | The shovel-sellers — the winners |

| Interchange | The card-swipe "toll" | Various card-issuing neobanks, Robinhood | Regulators pressing it down |

| Lending / consumer credit | Lending you money for interest | Affirm, Klarna, SoFi | Cyclical, thin margins |

| Net interest margin | The borrow-short, lend-long spread | Chime, SoFi (chasing deposits) | Needs scale to work |

| Cross-border FX | Swapping money across borders | Wise, Airwallex | The most fragmented, most expensive, easiest to route around |

II. Interchange: The Biggest Pool, Now Being Pried Loose at the Foundation

Let me first anchor the concept in plain terms — it's the least familiar to Chinese readers and the most consequential in America.

Interchange: every time you swipe a credit card in the U.S., the merchant is skimmed a "toll." That fee is cut into pieces, and the biggest piece goes to the issuing bank — which then uses that money to subsidize your points, cashback, and airport lounges. The whole American premium-card flywheel of "spend more, earn more" runs on this fuel.

In 2026, this fee pool saw its biggest tremor in twenty years: a merchant lawsuit that had dragged on for two decades finally reached a settlement with Visa and Mastercard, preliminarily approved in June by Judge Brian Cogan.

There's a trap here that both the writer and the reader can easily fall into, and we have to clear it up first: these are actually two different settlements. One is the cash settlement compensating for past losses, with a fund of US$5.54 billion, paid to merchants who overpaid on fees in the past; the other is a forward-looking fee-reduction settlement, priced at US$38 billion — but that US$38 billion isn't a lump of cash, it's "the cumulative amount merchants will save on interchange over the next five years." The terms of the latter are what truly move the foundation: credit-card interchange rates cut by 10 basis points over five years, standard consumer-card rates capped at 1.25% over eight years, and — for the first time — merchants allowed to selectively refuse the most expensive premium cards by card tier.

It sounds as if the foundation of the premium-card flywheel has been shaken loose. But the truly interesting part is the twist that follows — the flywheel won't collapse.

Why? Because merchants simply don't dare turn away their best customers at the checkout. In America, nearly nine-tenths of all credit-card spending happens on rewards cards, and this is precisely what gives the card networks the confidence to concede: they're betting that no merchant will shut out the crowd swiping top-tier cards — the highest-spending customers there are — just to save a sliver of fees. A more hidden layer: those 10 basis points that regulators fought so hard to squeeze out very likely never reach the merchant's hands — under the "bundled pricing" models of the likes of Square and Stripe, the saved spread is quietly pocketed by the payment processor, and only the big merchants on "cost-plus" pricing actually benefit. The small merchants, repeatedly "represented" by lobbyists on all sides, turn out to be the silent losers of this settlement.

In fact, this "two-sided market" logic was rubber-stamped by the U.S. Supreme Court back in 2018. That year, Ohio and a group of other state governments jointly sued American Express (Ohio v. American Express), arguing that its rule against merchants "steering customers to lower-fee cards" amounted to monopoly and pushed merchant fees too high. The Supreme Court ultimately ruled 5–4 that Amex hadn't broken the law, on exactly this reasoning: card-swiping is a "two-sided business" — one side the merchant, the other the cardholder — and you can't fixate solely on the fee the merchant is overcharged; you also have to weigh how much of that money subsidizes cardholders' cashback and benefits on the other side. Put plainly, the court effectively conceded that the whole two-sided network effect — "skim from merchants, use it to subsidize cardholders" — is legal, even efficient. So when regulators today try to pry this foundation loose through fee rates, they're prying at a model the Supreme Court itself endorsed — no wonder it's hard going.

Now look at China: this flywheel basically doesn't exist there. China's card-swipe fees are pressed extremely low by regulators, and are almost entirely routed around by the QR codes of Alipay and WeChat Pay — the two of which together account for over 90% of Chinese mobile payments. Once the payment gateway is taken over by two QR codes, the entire chain of "the issuing bank skims a toll, then uses the toll to subsidize points" has no soil to grow in. That's why the word interchange feels self-evident to Americans and nearly alien to Chinese — our generation essentially skipped the golden age of credit cards altogether.

III. Lending, Net Interest Margin, Cross-Border: Three Pools Defined by Cycles and Friction

Start with lending and consumer credit. The loudest number in the media is that Americans are carrying US$1.25 trillion in credit-card bills they can't pay off — which of course makes a great headline. But there's a counterintuitive fact worth putting on the table first: credit cards actually make up only 6.6% of Americans' total debt; the real bulk is mortgages, at 70%. In other words, the "credit-card debt crisis" is terrifying in the narrative but only a supporting player on the balance sheet.

The new players slicing into this pool are "buy now, pay later" (BNPL).

What's BNPL? It's that "4 interest-free installments" button on the checkout page — essentially splitting a purchase into a few installments of short-term credit. Think of it as the American version of Huabei and the various installment plans.

Affirm and Klarna are the poster children of this track. But you have to remember the underlying nature of this business: at heart it's lending, and it eats from the plate of the credit cycle. In 2021, Klarna was still losing about US$700 million with roughly US$500 million in bad debt (SEK 4.6 billion); and its valuation duly slid from US$45.6 billion that year all the way down to US$15 billion when it listed in 2025. Lending can grow fast, but it has never been a business that sails easily through the cycle — a point that will keep recurring in Section IV.

Here's a character Chinese readers know better: DiDi. In Latin America, DiDi has long been more than a ride-hailing app — it has laid out an entire fintech stack across the value chain: lending in Mexico (DiDi Préstamos, with over 20 million loans disbursed cumulatively, of which about 70% of users had never borrowed a cent before), issuing credit cards (DiDi Card, with Mexico its first card-issuing market worldwide, breaking a million cards in a single year), and adding BNPL (called DiDi Paga Después, i.e. "buy now, pay in installments"); in Brazil, its 99Pay arm plugged straight into the local instant-payment system, PIX. A company that started in ride-hailing went overseas and built lending, card issuance, BNPL, and payments end to end — which is exactly why BNPL has never been a business that can stand on its own; it's just one link in the full chain of consumer finance.

Now look at net interest margin — in plain terms, the spread a bank earns from "borrowing short and lending long": paying depositors low, charging borrowers high, and pocketing the difference. Its defining trait is that it's highly cyclical: in Q1 2026, the industry-wide net interest margin in the U.S. slipped 8 basis points quarter-on-quarter to 3.31%, while over the same period industry net profit was actually still rising, reaching US$80.5 billion. Profit rising while the spread shrinks — that very divergence is the fingerprint of the cycle. A business that lives on net interest margin has its lifeline held by interest rates, not by itself. Interestingly, that year consumer-confidence surveys fell to a decades-low trough, yet bank executives saw actual spending and borrowing that was quite robust — PNC's CEO flatly said he "can't reconcile those headline consumer-confidence surveys with what we see in our business every day; they're almost completely at odds." The real temperature of a fee pool is hidden in transaction data, not in questionnaires.

Now look at the most fragmented — and most expensive — piece on the map: cross-border FX.

Why is this pool so expensive? It's worth spelling out in plain terms (because it's precisely the pain point that the next piece's "shovel-sellers" set out to route around): a small or mid-sized bank isn't qualified to plug directly into another country's clearing system, so it can only open a "correspondent account" at a large bank — and as a result, every wire is charged a fixed fee of US$5 to US$50, millions of dollars of funds are forced to sit idle in non-interest-bearing overseas accounts, and a single system false alarm means another US$20 to US$100 "investigation fee." Look further up, and even SWIFT often gets blamed unfairly: the root of the slowness and cost isn't the SWIFT network itself, but the cutoff times of banks and various central banks.

Precisely because the friction of the traditional rails is absurdly thick, the players who came specifically to slice off this cut are living well. Wise (think of it as the player that made cross-border remittance both cheap and transparent — akin to the role LianLian and PingPong play in China's cross-border collection and payment on the individual and SMB side) posted 2026-fiscal-year underlying income of £1.61 billion, up about 18% year-on-year, serving roughly 18.9 million cross-border customers, driving its cross-border take rate all the way down to 52 basis points while still holding a 26% pre-tax profit margin — and in May 2026 it dual-listed on Nasdaq (with London remaining its primary listing), at a market cap of about US$12 billion. Its founder built the company years ago because of two people living in London — one holding pounds to pay off a mortgage in Estonia, the other holding krona to cover living costs in London — both fed up with the exchange-rate spread the banks kept hidden.

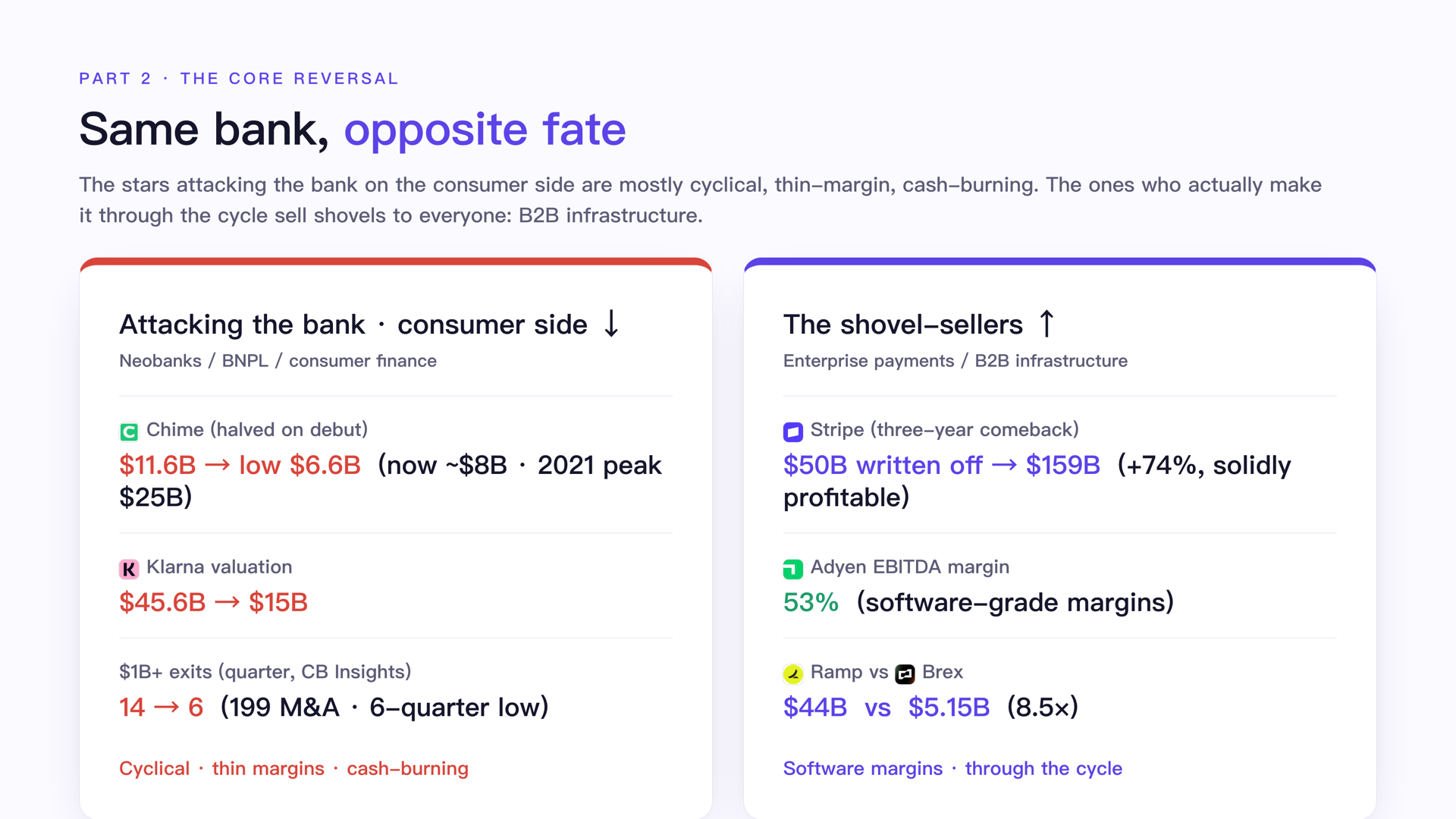

IV. The Twist: Those Attacking the Consumer Side Mostly Suffered; the Shovel-Sellers Kept Ascending

Now to the pivot of the whole piece. Lay two kinds of companies from the same window of time side by side, and the contrast is jarring enough to read almost like a fable.

First, the consumer side — those stars aiming directly at you and me, out to "remake a bank."

Their growth numbers are often gorgeous, but glance for a second at unit economics and valuation, and the story changes:

- Chime, the benchmark American neobank, listed in June 2025 at a market cap of about US$11.6 billion — which sounds substantial, yet that's already more than a 50% cut from its US$25 billion peak on the private markets in 2021; after listing, the stock kept sliding, at one point down to around US$6.6 billion, and now back to about US$8 billion. It did turn its first-ever GAAP profit in Q1 2026 with revenue up 25%, but the market is still only willing to hand it a very low valuation — effectively writing "thin-margin, highly cyclical consumer side" straight onto the price tag.

- Klarna, the European poster child of "buy now, pay later" (BNPL — in plain terms, Huabei-style installment spending), saw its valuation fall from US$45.6 billion in 2021 to about US$15 billion when it listed in September 2025 — two-thirds of its value evaporated in four years.

- Colder still is the price of exits. The door wasn't closed — Chime and Klarna both went public — but they squeezed out at prices cut in half and then in half again. Per CB Insights, in Q1 2026 there were only 199 global fintech M&A deals, a six-quarter low; large exits above US$1 billion fell from 14 in the year-earlier quarter to 6.

- The unit economics are more startling still: one licensed neobank (Varo) grew its account count by about half in a year, yet the deposits per account came to just US$52 — which all but confirms its customers are either living paycheck to paycheck or treating it as a dispensable side account; and Robinhood's premium card offering "unlimited 3% cashback on all spending," on the card-swipe itself, runs at nearly negative margin — per Flagship Advisory Partners' breakdown, each cardholder earns it no more than US$140 a year (and mostly from interest). The real recovery comes from membership fees, sticky assets, and the US$656 million a year in margin interest that Gold users pay. Put plainly, this is a "lose money to make noise" business — the cashback is the bait, and the money is made elsewhere.

Lay out the whole consumer-side table and it gets clearer: Chime around US$8 billion, SoFi around US$22.2 billion, Affirm around US$26 billion, Block (Cash App's parent) around US$44.3 billion — apart from Robinhood, hyped up to around US$101.5 billion by the frenzy around crypto and prediction markets (which is itself a signal of the cycle), most are below their own private-market peaks, or fall far short of the top-tier infrastructure.

(For reference: these neobanks = pure digital banks, with no branches, acquiring customers through an app and retaining them with small features like early payday deposit. The closest Chinese analogues are the C-end retail arms of WeBank and MYbank.)

The shared predicament of everyone at this table: growth bought by burning cash, profit propped up by cross-subsidy, valuation rising and falling with market sentiment.

Now look at the shovel-selling side — the companies that don't face consumers directly but provide the payment infrastructure for everyone.

Over the same stretch of time, they've been ascending to godhood:

- Stripe is the most dramatic reversal. In 2023, in that Shixiang report it was still being written off as in a "death spiral," its internal valuation at one point knocked down to US$50 billion and even that seen as steep; by February 2026, its latest round of employee equity transactions set the valuation at US$159 billion, up 74% from US$91.5 billion a year earlier. In 2025 it processed US$1.9 trillion in transaction volume, up 34% year-on-year, equivalent to 1.6% of global GDP, and was "solidly profitable"; even Microsoft routed "a substantial portion" of its volume to Stripe, and its client list includes Nvidia and Amazon. It also made its largest acquisition ever — buying stablecoin company Bridge for US$1.1 billion. That old "darkest before dawn" bet paid off.

- Adyen, Europe's payment-acquiring giant, posted full-year 2025 net revenue of €2.36 billion, up 21% year-on-year (at constant currency), with an EBITDA margin as high as 53%, targeting over 55% by 2028 — that's a software-company-level margin, not one a financial company should have.

- One contrast is especially glaring (the next piece will dig into it): both starting from the "corporate spend" track, the one that chose to build infrastructure, Ramp, is valued at US$44 billion, while the one that pioneered the category yet chose to be absorbed, Brex, was acquired by Capital One in 2026 for US$5.15 billion — the former is 8.5 times the latter's exit price.

Behind that fallen Parker from the opening lies an entire front of SMB (small and mid-sized business) banking, and the divergence of fortunes on this front is even sharper than on the consumer side. All providing accounts and corporate cards to small businesses: Parker went straight into liquidation and out; Brex, which pioneered the category, was absorbed by Capital One for US$5.15 billion in early 2026, becoming part of a big bank; Mercury took a third path — in late 2025 it simply applied for its own bank charter, aiming to go from "borrowing someone else's bank charter" to "being the bank itself," and now has over 300,000 customers and processed US$248 billion in transaction volume in 2025.

The most interesting is Slash: it started out issuing cards to "sneaker resellers" (a crowd with big cash flow who, being young and unincorporated, couldn't even get a decent bank card), then Kanye West's antisemitic remarks crashed the entire sneaker market, and Slash's revenue evaporated by 80% overnight; the two just-dropped-out founders wrenched the wheel and pivoted — going instead to build vertical banks for niche industries like marketing agencies, crypto companies, and even air-conditioning installers, reaching US$250 million in annualized revenue in 2025, and in April 2026 raising US$100 million at a valuation of US$1.4 billion. Look at that: on the same SMB-banking track, some liquidate, some get absorbed by a big bank, some simply go become a bank themselves, some survive by a single pivot — those who can "quietly survive, or even thrive," either marry into a big bank, or find an extremely narrow, extremely deep vertical no one else can be bothered to touch.

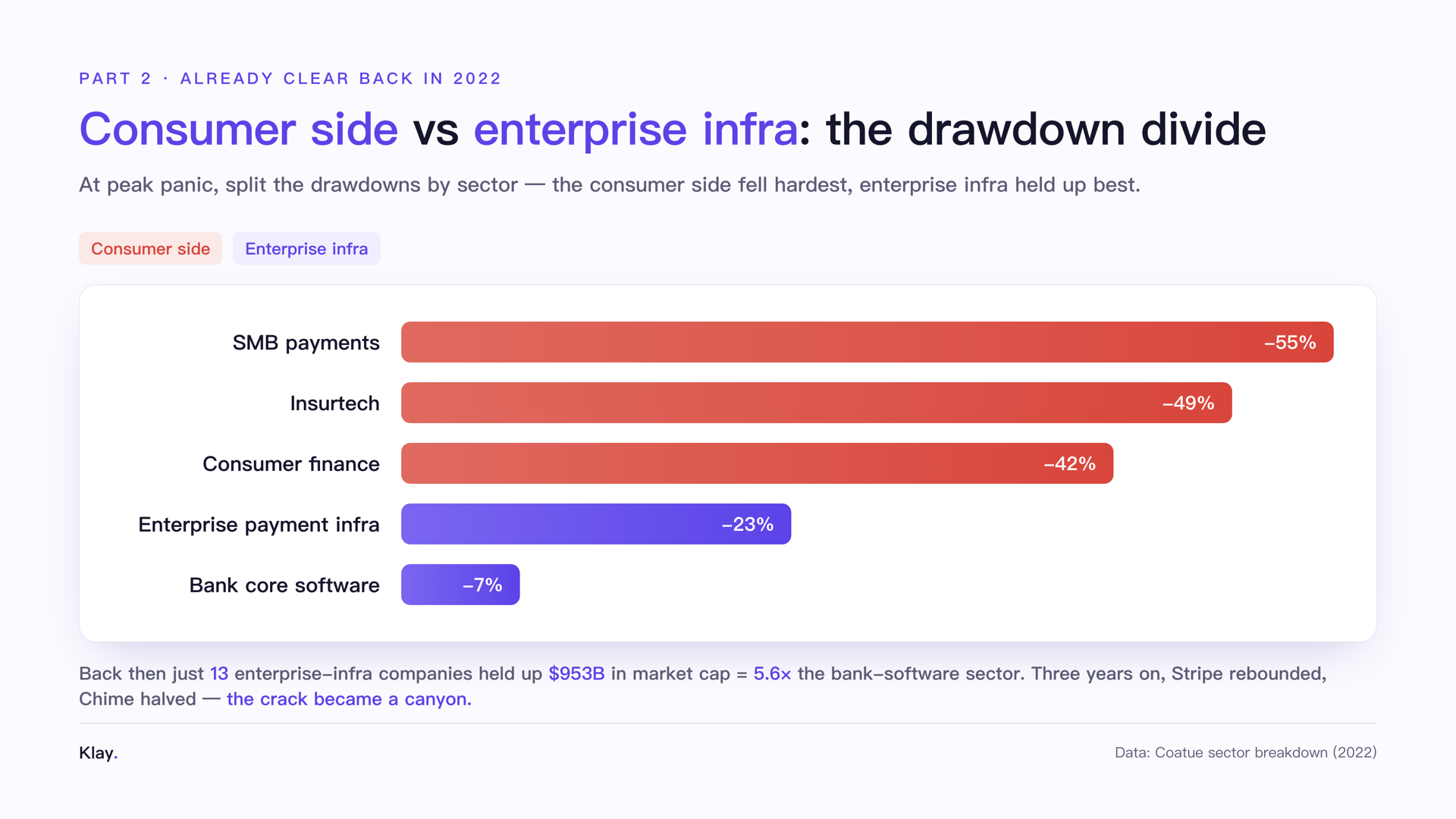

In fact, this fault line was already drawn crisply back in 2022, when the market was at its most panicked. That year Coatue broke down the declines of listed fintech companies by sector: consumer-side SMB payments fell 55%, insurtech 49%, consumer finance 42%; while enterprise payment infrastructure fell only 23% and bank core software only 7% — at the time, just 13 enterprise-grade infrastructure companies together held up US$953 billion in market cap, 5.6 times the entire bank-software sector. Three years on, this structure not only hasn't reversed, it's been borne out even more thoroughly by reality: on one side Chime listed at a 50% cut and Klarna at a 50% cut, while on the other Stripe went from being written off all the way back to US$159 billion. The fault line didn't heal; it became a chasm.

The divergence of fortunes between these two sides is no accident — it's priced by the market with a crystal-clear valuation logic. A Q1 2026 tally puts it bluntly: enterprise-grade infrastructure fintechs carry valuation multiples averaging 17x, the highest tier; while payments/transfers command only 7.7x. Why? Because the former has "software economics" (recurring revenue, plus customers that expand), whereas the latter's growth relies on piling on more transaction volume, bearing more risk and cost — so the market values infrastructure like "software" and values payments and consumer like "financial services." Another data point from the same period corroborates the same direction: of the largest B2B payment fundraises, enterprise-grade infrastructure took 60%.

This is exactly the continuation of last piece's key: in this industry, valuation has never tracked how much money you "handle," but how much you can "make" from it — and at what multiple you get priced. The consumer side that handles trillions yet drives fees to zero is worth far less than the infrastructure side that handles transactions yet squeezes out software-level margins.

V. A Devil's Advocate: Is the Consumer Side Really "Suffering"? Maybe It's Exactly the Thing to Attack

As is my custom, in this section I'll argue the other side in earnest — maxing out the case for the consumer side before returning to my own judgment.

The bull case, argued seriously: attacking the consumer side of banking is actually a pretty solid story.

First, it really can be profitable. Chime turned GAAP-profitable after listing, with revenue up 25% and over 10 million members. Second, it has the world's strongest counterexample — Nubank: this Brazilian digital bank is now valued at about US$62 billion, with over 131 million users, covering roughly 62% of Brazilian adults, the largest private financial institution in Brazil. It proves a pure digital bank can grow into a beast that swallows a traditional big bank. Third, the consumer side reaches the customer directly and comes with its own distribution, unlike infrastructure, which has to read the faces of big clients — the moment Cash App launched stablecoins, behind it sat a user base of nearly 60 million. Fourth, even the "super-app" story holds up: Robinhood is now valued at as much as around US$101.5 billion, far above the vast majority of consumer fintechs, and it's laundering its image from "gamblers' carnival" into "the younger generation's gateway to wealth." Fifth, that scary "great deposit exodus" never happened either — Coinbase paid stablecoin holders over 4% yields for nearly three years, the promised deposit outflow simply never materialized, and over the past two years total U.S. bank deposits have actually risen.

Let me add one analogy for the other side: the Brazilian version of Google is still Google, but the Brazilian version of "JPMorgan" is Nubank — in emerging markets, homegrown C-end digital banks aren't impossible to build; they've slapped the original version flat on the beach. So betting on the consumer side isn't foolish.

But back to my judgment: this bull case slams into three walls — unit economics, valuation multiples, and the exit environment.

Take apart the two sexiest counterexamples first. Nubank's success is in large part Brazil's high-interest-rate dividend, not tech magic — in a country where the benchmark rate is routinely in the double digits, feasting on the deposit-lending spread alone is enough to grow a beast; move that model to a low-rate mature market and it fails instantly. Robinhood's high market cap is just as fragile: its profit still depends heavily on trading — especially on the extreme-cycle species that is crypto — and the moment the market chills and crypto drops, the profit shows its true form; and its new bet, prediction markets, has the regulatory sword of "is this a financial instrument or gambling in disguise?" hanging over its head.

Now the three walls. Unit economics — Varo's US$52 in deposits per person, Robinhood Gold cards earning under US$140 per account a year (Flagship's breakdown) — this kind of business is inherently propped up by cross-subsidy. Valuation multiples — the market only grants the consumer side the low "financial services" multiple (7.7x), reserving the high "software" multiple (17x) for infrastructure. The exit environment — Klarna's two-thirds of value evaporating in four years, Chime cut in half on listing, large exits above US$1 billion falling from 14 to 6 within a year — capital has already voted with its feet.

And what says it best is the choice of the consumer-side winners themselves: Chime, SoFi, and Mercury are all scrambling to get bank charters, because only by becoming a bank can they keep for themselves the spread they'd otherwise hand to a partner bank; the "second-wave neobanks" that can't reach this step can only wait to be absorbed by a super-app — which is precisely the opening of the story I'll tell in Part Four.

VI. Closing: After Unbundling, Who Crossed the Cycle?

Three sentences to close out this second piece.

First, the bank's fee pools are big and scattered, so everyone comes to attack them. Payments, interchange, lending, net interest margin, cross-border FX — each is a billion-dollar wedge in the U.S.; the worst legacy experiences leave the most openings. This was the most surging startup wave of the past decade.

Second, but the star companies attacking the consumer side of banking mostly went on to do quite poorly. Chime cut in half on listing, Klarna's two-thirds evaporated in four years, large exits falling from 14 to 6 within a year — they're mostly cyclical, thin-margin, cash-burning businesses, and a winner's fate is either to become a bank or to be absorbed by a super-app.

Third, the ones who actually crossed the cycle and quietly made the big money were a different crowd — the "people selling shovels." Stripe went in three years from being written off at US$50 billion to a solidly profitable US$159 billion, Adyen guards a software-level 53% margin, and the market — with a valuation gap of 17x versus 7.7x — has clearly priced "enterprise-grade infrastructure" and "consumer payments" as two different things.

So who exactly are these "people selling shovels," what makes their moats so deep, and how will the new rail of stablecoins rewrite the battle?

That's the subject of my next piece — "The People Selling Shovels: Stripe / Adyen / Airwallex."

Finally, a bonus: a physical exam of the American wallet — understand it, and you understand where the demand for BNPL and neobanks grows from.

(Data in this piece uses the most recent figures available as of 2026: Parker's Chapter 7 filing on May 7, 2026, its would-be acquirer Avalara and the roughly US$90 million deal, and the US$200 million in funding including a US$125 million lending facility come from public reporting; Ohio v. American Express is the U.S. Supreme Court's 2018 5–4 ruling; DiDi's Latin America lending / card-issuance / BNPL figures come from public reporting; Brex's US$5.15 billion acquisition by Capital One, Mercury's bank-charter application and US$248 billion in transaction volume, and Slash's US$250 million annualized revenue and US$1.4 billion valuation are all public disclosures; Stripe's US$159 billion valuation and US$1.9 trillion transaction volume come from its 2025 annual letter and February 2026 employee equity transactions; Adyen figures come from its full-year 2025 shareholder letter; Chime and Klarna market caps and IPO figures come from public-market disclosures; the two Visa/Mastercard settlement amounts are, respectively, the US$5.54 billion cash fund and the US$38 billion five-year cumulative fee reduction; the 199 fintech M&A deals and the 14→6 drop in US$1B+ exits come from CB Insights' State of Fintech Q1 2026; the Robinhood Gold card unit economics (US$140 / US$656 million) come from Flagship Advisory Partners' breakdown. Listed-company market caps are as of June 2026 and will fluctuate with the trading day.)